Whose Gate Do You Pass Through? AI Hits the Hard Limits of Chips, Power, and Politics

IN THIS ISSUE:

CEO's Perspective

Strategic outlook from Cambrian leadership

On April 12, in a channel of the Institute of Sovereign Investors, I argued what I believed to be an unpopular position: any war-ending deal would need a permanent, shared toll booth in the Strait of Hormuz, run like the Suez Canal. The U.S. does not need the oil and American consumers absorb less of the cost, so the White House would have leeway to direct its share of toll revenue toward Iranian reconstruction and the replenishment of U.S. munitions. A revenue-positive war is a politically usable war. The toll booth went up last week, but whether the U.S. will participate remains to be seen when a final deal gets negotiated. It might be a bridge too far.

The Toll Booths Went Up

It’s not the only toll booth to emerge in recent weeks. The U.S. Department of Commerce said it believes one of ASML’s extreme ultraviolet (EUV) lithography machines slipped into China. Commerce presented the claim without evidence and asked The Hague to enforce it, and now 20% of ASML's 2026 revenue sits on the answer. At Évian, the G7 built a critical-minerals bloc against China's processing chokehold, and then discovered at the same lunch that the export controls used last week to switch off Anthropic's frontier models could switch off any model whenever Washington chose. Macron promised a Western AI platform within a month – the sort of thing you say when the toll booth you assumed was on someone else's road turns out to be on yours. In one week, three different chokepoints on the AI stack got priced or repriced. A literal toll on the energy that powers compute. A geopolitical premium on the equipment that prints the silicon. A switch in Washington that gates allied access to the models themselves.

The other two stories in this week’s Radar have a similar theme. The Justice Department moved to shield xAI's Memphis turbines from environmental law on national-security grounds, which is what owning a chokepoint looks like when the chokepoint is yours and the toll is paid in the local air. OpenAI's leaked books, with $25 billion in cash and a confidential S-1 already filed, weaken Washington's case for an equity stake in the labs, but they do not eliminate it. The federal toll booth on AI is not closed. It is being negotiated. Two weeks ago this letter argued the money had met the wall. The wall turns out to be a row of toll booths with named owners, and the owners are charging.

If nothing else, leaders who see these toll booths need to stop assuming open access at any layer of the AI dependency chain. Map the chokepoints. Name the owners. Price what each one is charging or is about to charge – on equipment, compute, models, minerals, energy, and capital. The era of frictionless inputs is over. The question is no longer how much compute you can buy. It is whose gate you have to pass through to use it and what the toll has been set at this week.

Olaf

On the Radar

The signals affecting the GeoTech landscape this week

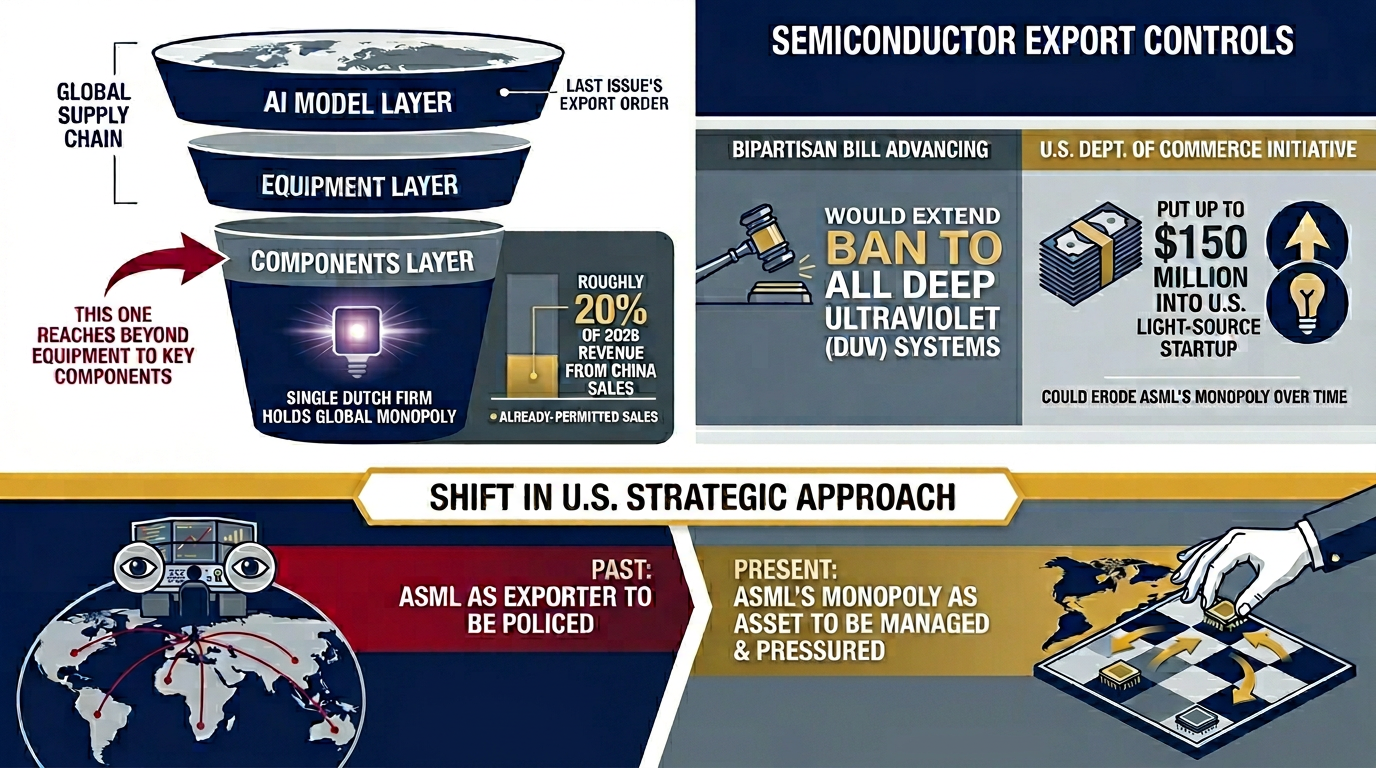

The Missing Scanner: Commerce Confronts ASML Over an EUV Machine in China

The U.S. says one of the world’s most tightly controlled machines might have slipped behind the line it was built to hold. ASML says that is physically impossible.

TL;DR: U.S. Commerce Secretary Howard Lutnick has told ASML he believes one of its extreme ultraviolet (EUV) lithography systems may have reached China. The company flatly denies it, and officials have not produced the evidence. The accusation escalates the older, parallel fight over chipmaking equipment that runs alongside last week’s controls on the AI models themselves.

BRIEFING: In a series of private meetings, U.S. Commerce Secretary Howard Lutnick warned senior ASML leaders that he believes one of the company’s EUV lithography machines may have entered China in breach of controls in place since 2019. ASML rejected the claim outright, noting that an EUV system is the size of a school bus, weighs some 180 tons, needs constant on-site servicing by ASML staff, and is tracked by remote telemetry, so it cannot be relocated unnoticed. Officials say they hold evidence of EUV-related component and transport shipments but have declined to show it, to ASML or to reporters.

These are parallel fights, and the equipment one is older. The drive to deny China advanced chipmaking tools runs back through the 2022 CHIPS and Science Act and the 2019 ban on selling ASML’s EUV machines, the most advanced lithography tools and the only ones capable of printing leading-edge logic. ASML is their sole maker. By contrast, Japan’s Nikon and Canon compete only in older deep ultraviolet (DUV) systems, which pattern mature and trailing-edge chips and which China can still buy, the roughly 20% of 2026 revenue now in play. The escalation runs on two tracks. A bipartisan bill, the MATCH Act, would extend the ban to all DUV sales to China, and the same Commerce Department pressing ASML has put up to $150 million into xLight, a U.S. startup building a free-electron-laser light source that could one day challenge ASML’s monopoly. The U.S. has stopped treating ASML purely as an exporter to be policed and started treating its monopoly as a strategic asset to be managed, and pressured.

SO WHAT

For Executives: Advanced-chip capacity rests on a single equipment supplier with no real alternative, and a widened DUV ban would tighten that bottleneck. Treat it as a live planning scenario, not a tail risk: map where your roadmap depends on ASML-served fabs, and stress-test what the loss of China-bound DUV capacity does to industry-wide lead times and wafer pricing. The hedges are unglamorous but real, including qualifying second-source capacity at mature nodes, pre-committing to fab allocations earlier in the cycle, and shifting designs toward nodes that do not require leading-edge lithography. Firms that price lithography access as a strategic risk now, before a ban lands, will keep their roadmaps intact when competitors are scrambling for wafers.

For Policy Makers: The sharpest read is from The Hague, not the government pressing the case. The Netherlands and the EU are being asked to enforce a claim the U.S. has presented without public evidence, which tests how much sovereignty allied governments retain over their own industrial champions once a technology is deemed strategic. Dutch Prime Minister Schoof has already raised ASML’s position directly in U.S. meetings, and the harder question is whether the EU forms a common stance or lets each member negotiate alone and be picked off. Build contingency positions now, because the precedent set here will govern the next allied company caught between U.S. security demands and its own commercial autonomy.

For Investors: ASML’s roughly 20% China revenue exposure is the near-term variable, though analysts at Quilter Cheviot put the net hit nearer 5% once the China share of DUV is isolated, so the headline risk likely overshoots the model. The slower and larger threat is erosion of the monopoly premium that underwrites the stock, which is why the state-funded xLight effort matters more than its dollar size suggests. Expect equipment-sector volatility on every disclosure, and treat the MATCH Act’s progress as the binary catalyst to track. Position for a long monopoly under rising political friction, and watch for next-generation light-source and DUV challengers that could re-rate the whole sector late this decade.

For Service Providers: European industrial champions caught between U.S. pressure, legitimate allied concern over China’s access to Western equipment, and their own commercial autonomy face a genuine messaging problem. The task is to defend compliance and reputation without appearing to either defy or capitulate to U.S. demands, and to do it for three audiences at once: regulators in The Hague and Brussels, customers in Asia, and a U.S. administration that is at once accuser and funder of a competitor. Anchor the narrative in verifiable compliance, where ASML’s ability to account for every installed machine through telemetry is a concrete asset, rather than in rhetoric. Clients in this position should war-game the disclosure scenarios before the next leak forces an improvised response.

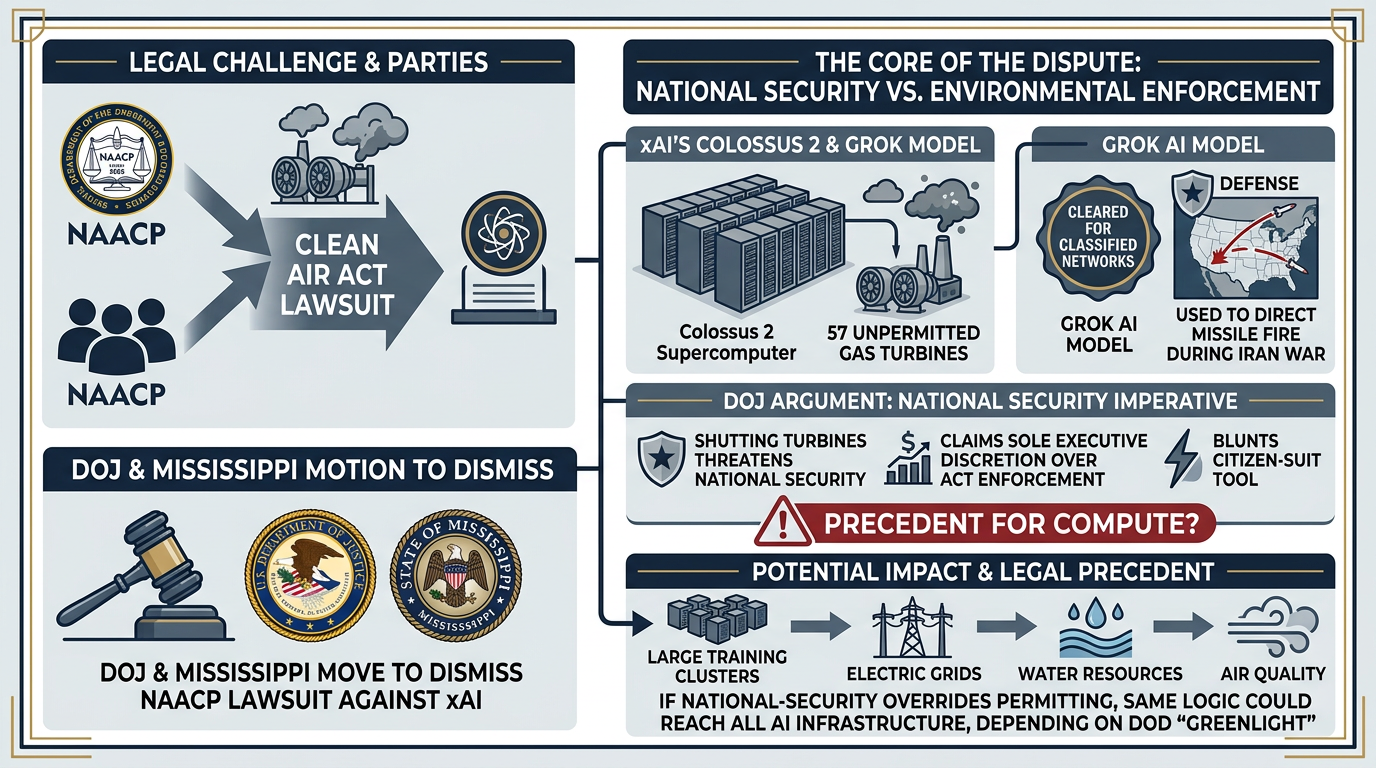

Too Vital to Switch Off: The Justice Department Shields xAI’s Memphis Turbines

A civil rights suit over unpermitted gas turbines has become a test of whether AI compute now counts as national-security infrastructure.

TL;DR: The Department of Justice moved to dismiss the NAACP’s Clean Air Act suit against xAI’s Memphis-area turbines, arguing a shutdown would threaten national security. The filing revealed that Grok runs on classified military networks and was used in the Iran war. The case asks whether compute now sits above ordinary law.

Briefing: The Department of Justice (DOJ) and the state of Mississippi moved to dismiss a Clean Air Act lawsuit brought by the National Association for the Advancement of Colored People (NAACP) against Elon Musk’s xAI, which has run as many as 57 unpermitted gas turbines near Memphis to power its Colossus 2 supercomputer. The DOJ argued that shutting the turbines would threaten “American national, economic, and energy security,” and a Department of War declaration disclosed that Grok is one of only four models cleared for classified networks and was used to direct missile fire during the Iran war. The department also claimed sole executive discretion over when to enforce the Act, a position that would blunt the citizen-suit tool communities have relied on for half a century.

The case matters because it converts a local pollution dispute into a precedent about the legal status of compute. If national-security necessity can override environmental permitting and private enforcement, the same logic potentially reaches every large training cluster and the grids, water, and air around it, depending on whether an AI model has been greenlighted by the Department of War. It also surfaces a tension the build-out has so far avoided. The megawatts are physical, sited in real neighborhoods, and the residents nearest them, in this case predominantly Black communities already burdened by poor air quality, carry costs that classified benefits do not offset. The rationale of this particular case is American, yet every government racing to host sovereign compute could plausibly reach the same collision between strategic priority and local consent.

So What

For Executives: Data-center siting has become a political act, governed as much by community consent as by land and power prices. Expect environmental-justice opposition to become a standard gate on large clusters, and budget for the legal, permitting, and reputational costs that follow rather than discovering them mid-build. Play through both outcomes of disputes like this one, national security prevailing and national security failing, because each carries a different planning risk for anyone siting or financing capacity. The operational lesson is to lock in permitted, grid-connected power and genuine community agreements early, since the cheapest, dirtiest option becomes the most expensive once litigation and local opposition attach.

For Policy Makers: The precedent worth watching is the reclassification of hybrid private-public compute as critical national-security infrastructure. Other governments will weigh whether to grant similar carve-outs from environmental and administrative law, and they will discover what that trade does to public trust, internal security, and economic development. The deeper hazard is that the same logic, national security overriding citizen enforcement, can be invoked by any state for any favored builder, with a preliminary-injunction hearing set for late August as the near-term test of how far courts will let it run. Decide where the line sits before the case law hardens, because litigating it cluster by cluster cedes the precedent to whoever moves first.

For Investors: A durable national-security shield lowers shutdown risk for sited compute assets, which is bullish for power-secured capacity and for operators that can credibly claim a defense nexus. The offsetting risk is litigation and reputational exposure, concentrated for now in xAI and its parent, and the late-August injunction hearing is the catalyst that prices it. Assess the alpha and beta implications accordingly, because the asset-level protection is real but the headline risk travels to anyone financing trailer-mounted, unpermitted generation. Against this backdrop, compliant grid-connected power looks underpriced relative to the litigation tail on the cheap-and-dirty route.

For Service Providers: Clients hosting compute must reconcile a classified national benefit with a visible local cost, a message that fails the moment it dismisses the affected community. The work is to separate the defensible claim, that compute can be genuine national infrastructure, from the indefensible posture, that clean-air law is therefore optional, and to steer clients away from the latter even when the government is offering air cover. Clients all the way downstream of compute will want robust strategic and public-relations positioning before the next emissions story breaks. The tightrope runs between national security on one side and environmental-racism allegations on the other, and saying nothing reads as the wrong answer.

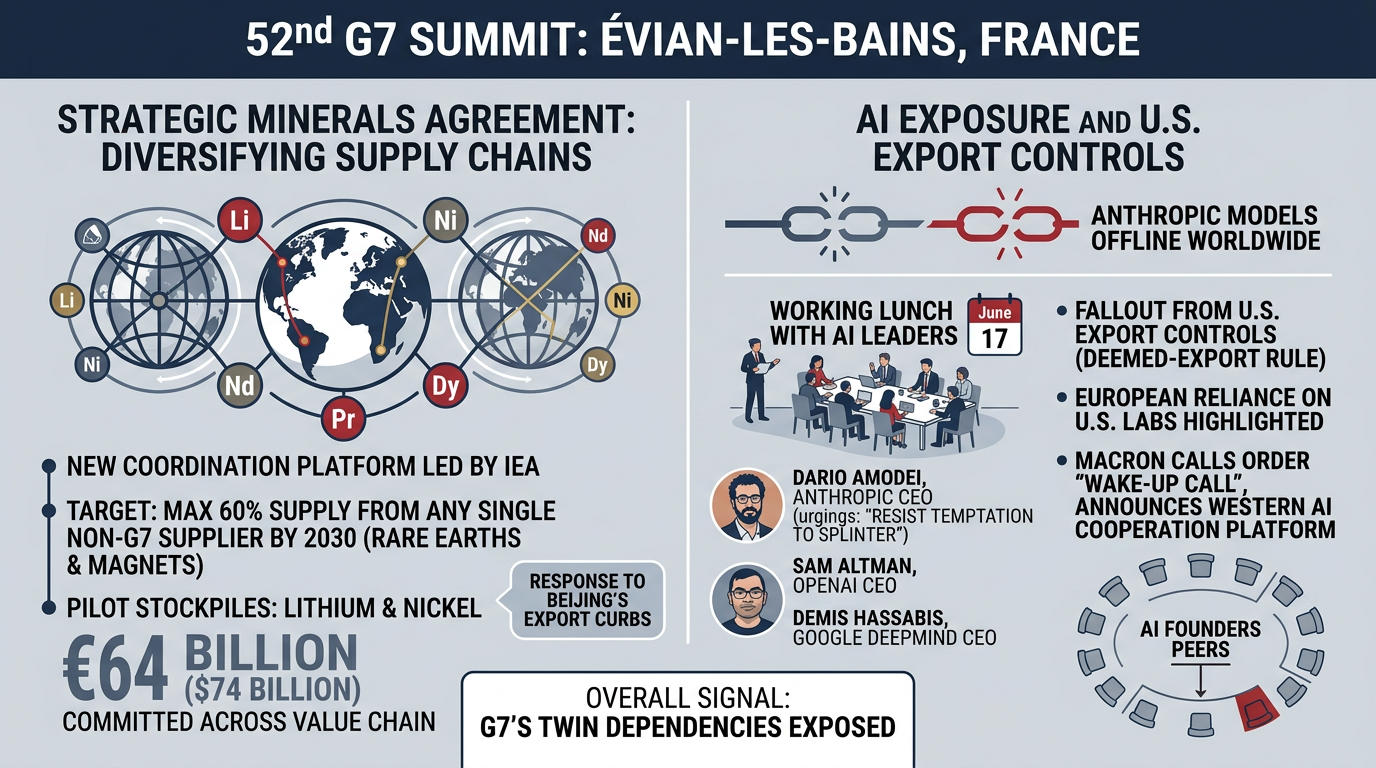

Évian’s Two Dependencies: The G7 Moves Against China’s Minerals and Reels From America’s AI Controls

The same summit that forged a minerals bloc to escape China found it had no answer to U.S. controls on Anthropic’s models. The G7 leaders learned just how easily an ally can be switched off from frontier AI.

TL;DR: The G7 meetings in Évian produced a critical-minerals bloc against China, an International Energy Agency-led platform targeting less than 60% reliance on any single supplier by 2030. However, U.S. controls that knocked Anthropic’s Fable 5 and Mythos 5 offline worldwide showed the American allies how easily their frontier-AI access can be cut, making natural resource security less impactful. Macron promised a Western AI platform within a month.

Briefing: At the 52nd G7 summit in Évian-les-Bains, France, leaders agreed to a critical-minerals framework built around a new coordination platform led by the International Energy Agency (IEA). The agreement intends to keep any single non-G7 supplier below 60% of rare earth and magnet supply by 2030, and it pilots stockpiles of lithium and nickel with roughly €64 billion ($74 billion) already committed across the value chain. The summit was overshadowed by the fallout from U.S. export controls that days earlier had forced Anthropic to take its Fable 5 and Mythos 5 models offline worldwide, cutting off allied users, a development one policy researcher called a “key topic” of the AI conversation. On June 17, the chief executives of OpenAI, Anthropic, and Google DeepMind joined leaders for a working lunch, where Anthropic CEO Dario Amodei urged the group to “resist the temptation to splinter.”

Leaders also agreed a set of principles for protecting minors online, the multilateral umbrella over the national under-16 bans already live in Britain, Australia, and Indonesia. But the harder lesson was the dependency exposed. On minerals the G7 moved with rare unity, answering Beijing’s export curbs with a coordinated buyers’ bloc, the multilateral successor to the bilateral framework we covered in Issue 22. On AI it could only register its exposure. Because the U.S. treats access by any foreign national as an export, a restriction aimed abroad became a global shutdown, and European leaders discovered that their reliance on three U.S. labs had become an operational fact. Macron called the order a wake-up call while warning that the limits themselves were damaging, and announced a Western AI cooperation platform to be established within a month.

So What

For Executives: Plan for both dependencies at once, on the critical minerals upstream and on the AI models built on top of them. Relief for the minerals risk is now in motion through the IEA platform, but the model-access risk is not, and it is the one that can interrupt operations overnight. Frontier-AI access has become a geopolitical variable, so assume any single-vendor, single-jurisdiction dependency can be switched off by export action, and build real portability across providers, open-weight fallbacks, and regions into anything mission-critical. The firms that dismissed multi-model redundancy as over-engineering just watched it become basic risk management.

For Policy Makers: This is the European sovereignty case made concrete, and the child-online-protection principles agreed at Évian now sit above the national under-16 bans live in Britain, Australia, and Indonesia. The open question is whether Macron’s one-month platform yields real shared infrastructure and a trusted-partner access regime, or whether allies simply accelerate domestic alternatives. In our view, competitive sovereign capacity cannot be built and operationalized within that timeframe, so interim dependence will persist even as the politics harden. The real decision for each capital is whether to negotiate access guarantees with the U.S. or to subsidize home-grown capacity, because hedging both halfway leaves a country exposed on both.

For Investors: The episode is a tailwind for European and sovereign-AI builders, for open-weight ecosystems, and for compute that sits outside U.S. jurisdiction. It also flags that the leading U.S. labs carry policy risk that can strand allied customers overnight, even as the voluntary-commitment path shields the labs themselves from binding rules. Given the projected need for steadily rising global compute, the question becomes not whether but when to fund European and other regional build-outs, with the Macron platform as the policy signal to track. On minerals, the IEA platform and its offtake and stockpiling commitments point capital toward non-Chinese extraction, processing, and recycling.

For Service Providers: A direct brief for a European communications firm: clients now need contingency narratives for AI-access disruption and clear positioning on digital sovereignty, the kind of plan written before a shutdown rather than during one. The same clients face the child-online-protection principles agreed at Évian, which sit above the national under-16 bans and will land next on EU platforms, including in Germany. Help clients hold two messages at once, credible support for democratic AI governance and honest contingency planning for the day access is gated. The firms that rehearse the disruption story now will not be improvising in front of regulators and customers later.

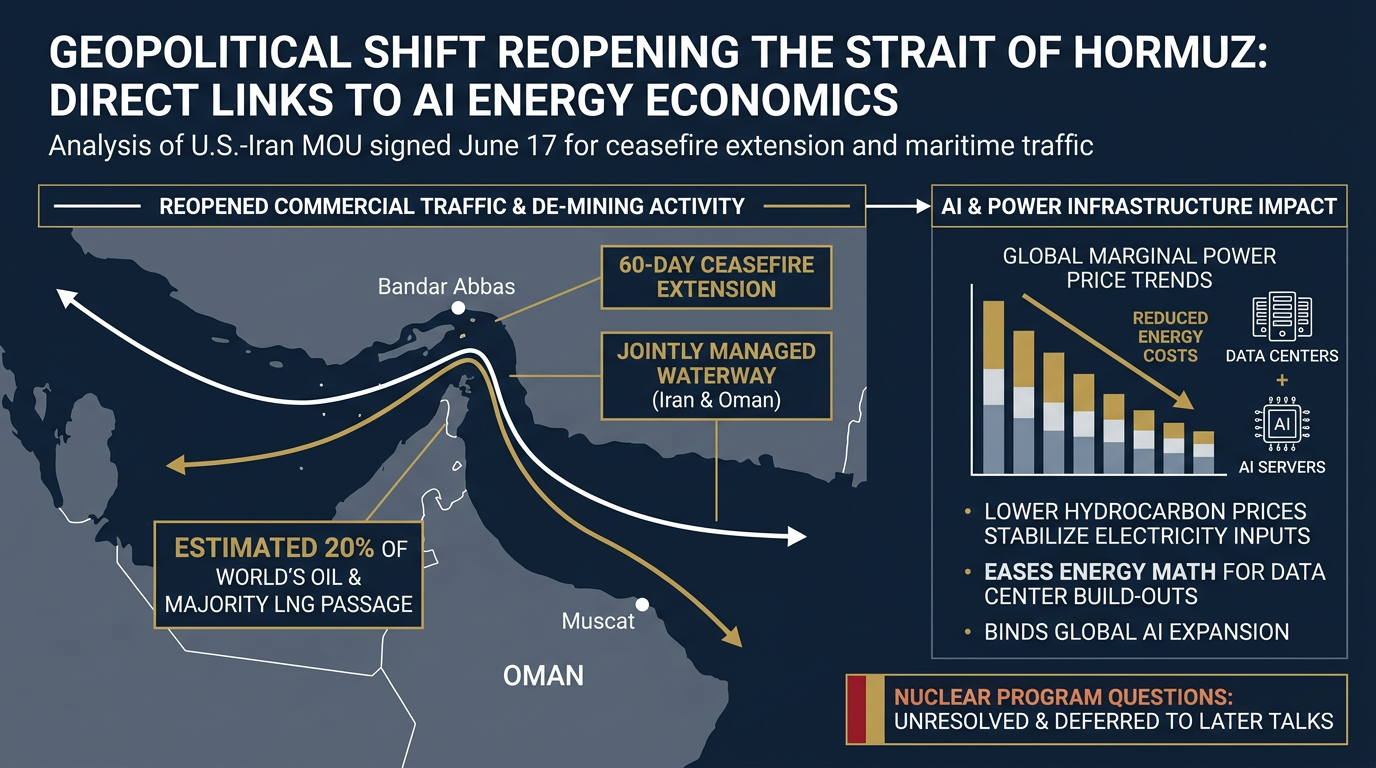

Hormuz Reopens: Cheap Crude, Gulf Tolls, and the Power Bill for AI

The strait that carries a fifth of the world’s oil is reopening, and the terms set a floor under the cost of running data centers everywhere.

TL;DR: The U.S. and Iran signed a memorandum of understanding that extends their ceasefire 60 days and reopens the Strait of Hormuz, with Iran and Oman set to manage passage and charge fees. Energy is the substrate of AI compute, and this deal moves its price. However, the relief could be temporary if the opposing sides do not reach a final deal on Iran’s nuclear capacities.

Briefing: This week the U.S. and Iran signed the Islamabad memorandum of understanding (MOU) to extend their ceasefire 60 days and reopen de-mining and commercial traffic through the Strait of Hormuz, the route for roughly 20% of the world’s oil and much of its liquefied natural gas. The strait reopens toll-free for the 60-day window only, after which Iran has said it will manage the waterway jointly with Oman and “charge fees for services,” a stance that cuts against the permanently toll-free passage the U.S. had pledged. Questions about Iran’s nuclear program remain unresolved and deferred to later talks, and the closure and U.S. blockade that preceded the deal had driven fuel prices sharply higher and rippled throughout the global economy.

Electricity is the binding input on AI’s expansion, and a meaningful share of the world’s marginal power still tracks Gulf hydrocarbon prices. A reopened Hormuz lowers and steadies that input, easing the energy math behind every data center build-out from Texas to the Gulf. The terms matter more than the reopening itself. An eventual Iran-Oman toll turns a free passage into a priced one and hands Tehran a recurring lever over the energy that powers the compute race, at the very moment that Gulf states are positioning themselves as sovereign-compute hosts. As the Council on Foreign Relations notes, states that can bypass the strait by pipeline gain an edge over Kuwait, Qatar, and Bahrain, which cannot. By Eurasia Group’s reading, the war accelerated a regional realignment in which energy leverage and AI ambition increasingly run through the same actors.

So What

For Executives: Energy, and its geotech implications, is now a board-level variable for compute-heavy operations. A calmer Hormuz improves the near-term cost outlook, but the reopening is toll-free for only 60 days, after which an Iran-Oman fee regime is on the table. That argues for hedging Gulf exposure rather than assuming cheap, frictionless supply, and for writing energy-price and transit-risk clauses into compute and offtake contracts that will face periodic renegotiation. Treat this as a reprieve to use, not a return to normal.

For Policy Makers: As we noted previously, the compute map is rebalancing from consumer-proximity toward energy-proximity, and this deal accelerates it. The same states that supply the world’s oil are bidding to host its compute, and Iran’s prospective toll gives Tehran leverage over both, while Gulf states that can route around the strait gain an edge over those that cannot. Energy security and compute security are converging into one portfolio, and the 60-day clock makes that convergence urgent. Plan sovereign-compute and energy policy together, because the same waterway now prices both.

For Investors: Expect oil-price normalization to ease input-cost pressure on data centers and energy-intensive AI, but only if the sides reach a permanent deal inside the 60-day window. For now there is a residual risk they do not, and a nuclear breakdown would re-close the strait and spike power costs again. Gulf sovereign-compute plays, shipping, and marine insurance are the clearest places where the reopening temporarily reprices risk, with the toll question the swing factor on Gulf-routed cargo. Size positions for a fragile, time-boxed truce rather than a settled peace.

For Service Providers: Clients with Gulf energy or infrastructure exposure need a steady strategy and narrative to navigate a fragile ceasefire that could reverse on a single nuclear-talks headline. The reputational tightrope is engaging an Iran-linked toll regime without owning its politics, especially for clients whose U.S. and Gulf stakeholders read the same deal differently. This is a portfolio strategy issue for any client, not a one-off statement. Build the message now and pre-clear it, because the 60-day window guarantees more headlines.

Under the Radar

The deep analysis that connects the dots

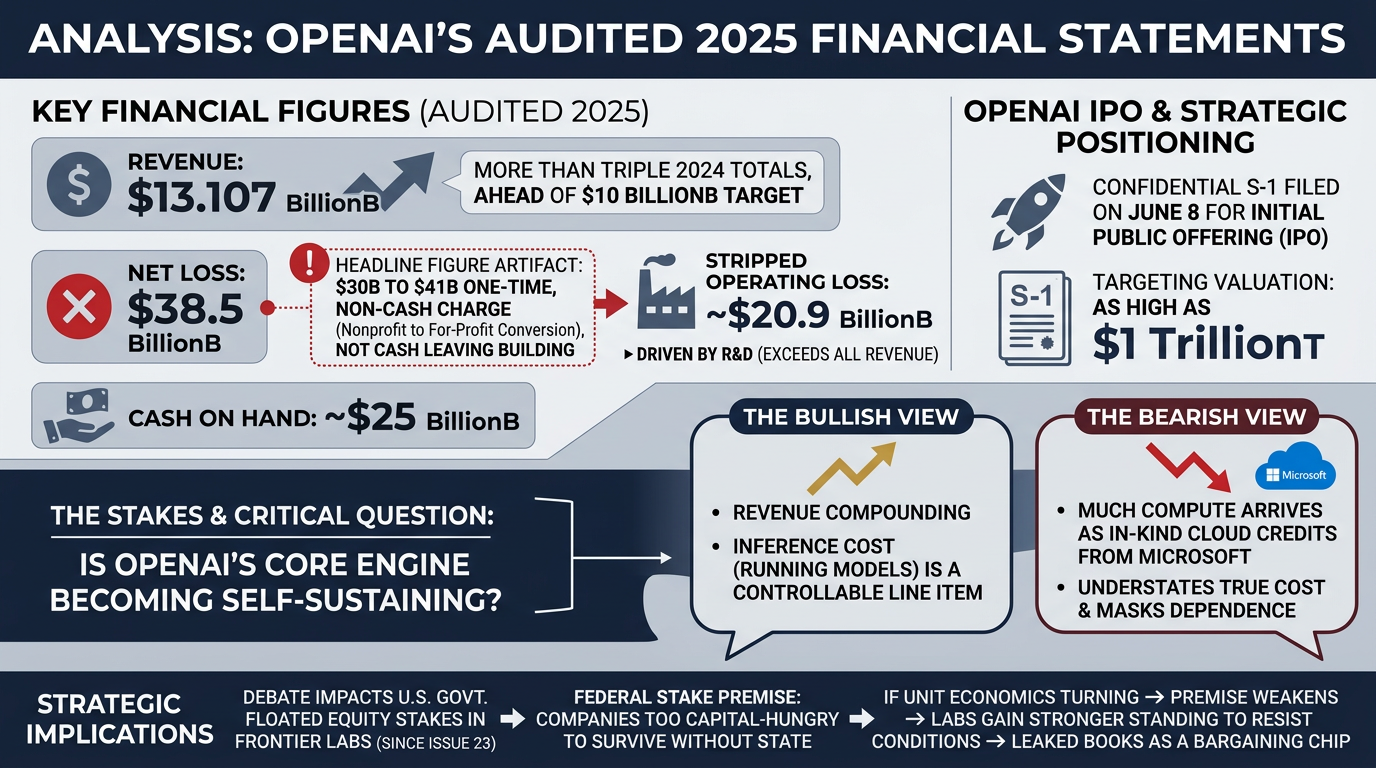

The $38.5 Billion Misread: OpenAI’s Books and the Case Against a Federal Stake

OpenAI’s leaked 2025 books show a $38.5 billion net loss on tripling revenue. The figure that decides what it means is the operating loss underneath it.

The Signal

Audited 2025 financial statements obtained by journalist Ed Zitron and verified by the Financial Times show OpenAI with revenue of $13.07 billion, more than triple 2024 and ahead of its own $10 billion target. The company spent about $34 billion to earn it, for an operating loss of $20.92 billion, with research and development of $19.18 billion alone exceeding all revenue. The far larger $38.5 billion net loss is a different animal, inflated by a one-time, non-cash charge tied to the October 2025 conversion to a public-benefit corporation. The Financial Times puts the comparable adjusted loss at roughly $8 billion once those one-time items are stripped out. OpenAI filed a confidential S-1, the registration that precedes an initial public offering (IPO), on June 8, targeting a valuation as high as $1 trillion, and it sits on roughly $25 billion of cash.

THE STAKES

The documents raise a more critical issue than the headline revenues or losses, namely whether OpenAI’s core engine has become self-sustaining. Analysts reading the same numbers split hard. The bullish view notes that revenue is compounding while the cost of inference is a line the company can control, since cost of revenue ran about $7.5 billion against $13.07 billion of sales. The bearish view notes that much of OpenAI’s compute arrives as in-kind cloud credits from Microsoft, which understates the true cost and masks dependence. That dispute lands on a thread we have tracked since Issue 23, when the U.S. government floated taking equity stakes in frontier labs. The case for a federal stake rests on the premise that these companies are too capital-hungry to survive without the state. If the unit economics are turning, that premise weakens, and the labs gain a stronger standing to resist the conditions a federal investor would attach. Read this way, the leaked books are a bargaining chip.

What to Watch

Three markers will show which reading is right. First, the gross margin OpenAI discloses in its eventual prospectus, the first audited look at whether inference pays for itself once cloud credits are priced honestly. Second, whether the federal-equity conversation survives contact with a $1 trillion private valuation and a $25 billion cash pile, or quietly fades. Third, whether rivals’ numbers, with SpaceX’s prospectus already showing a different profile, push investors to reward proven inference economics over headline growth. For operators and investors, the practical move is to discount the loss figure and wait for the margin line. It is the only number in this story that settles the argument.

About Cambrian

Cambrian Futures is a strategic foresight and advisory firm helping government, business, and technology leaders understand how emerging technologies intersect with geopolitics, markets, and national strategy. By combining rigorous research, AI-enabled analysis, and human expertise, Cambrian provides clear insight into global technology trends, risks, and power dynamics. Its work helps decision-makers anticipate disruption, manage uncertainty, and act with strategic confidence in an increasingly competitive GeoTech world.

PRODUCTION TEAM

GeoTech Radar is produced by the Cambrian Futures Insights Platform team:

CEO & Chief Analyst

Managing Director / Producer, Insights Platform

Global Lead, Smart Infrastructure Strategy

Research & Marketing Associate

Editor in Chief

Learn more about Cambrian Futures at cambrian.ai

Produced with

Human Led

Human Led +

AI Augmented

AI Led +

Human Verified

Cite as: Cambrian Futures (2026) 'GeoTech Radar Issue 25'

An important note on what this is, and is not

GeoTech Radar is directional research intended to stimulate thinking and provide geopolitical and technological context. It is not investment, legal, or financial advice, and nothing here is a recommendation to buy, sell, or hold any security or asset. The companies, valuations, and transactions discussed are described for analytical context only and serve as a backdrop to readers' own due diligence. Figures and claims are drawn from public reporting as of the publication date and may change. Readers should consult their own qualified advisers before making any decision. Cambrian Futures and the authors hold no responsibility for actions taken on the basis of this briefing.