Washington Buys In as the Labs Cash Out. Anthropic Pulls the Brake. Compute Runs Dry.

IN THIS ISSUE:

CEO's Perspective

Strategic outlook from Cambrian leadership

This past week I co-taught a session of my new executive course "Frontier AI Ventures for Air, Space, Sea and Arctic" with a Berkeley venture finance professor on my advisory board, showing entrepreneurs how to raise money for Physical AI ventures that open new economies and industries. Getting the funding is always the near-term goal. What we kept returning to is what happens after the money arrives. It meets walls, fast: unforgiving physics, purpose-fit hardware, the politics, geopolitics and economic externalities of natural resources, scarce expertise, and social equity.

The Money Has Met the Wall

Read across this issue and the inversion becomes clear. For two decades capital was the binding constraint on tech. AI has flipped the order. Money is now the most abundant input on the table. The state wants equity in the labs, the public market is being asked to absorb the largest listings in history at fixed prices before the roadshow even starts, and a senator wants half. Meanwhile over sixty percent of planned U.S. data center capacity for 2027 is not yet under construction, transformer lead times have stretched from under a year to four, and Google is renting GPUs from a rocket company at nearly a billion dollars a month. Money buys announcements, not megawatts.

The wall is not only physical, though that part is the most visible. Each query spends a bottle of water, and the basins with the cheapest power and sovereign capital are often the ones with the least of it. The magnets behind the motors are still processed almost entirely in China, and the firms betting hardest are quietly trying to engineer rare earths out of the magnet, because matching China at its own game is harder than walking around it. Then there is the wall the labs are putting up themselves. Anthropic named chip fabrication, grid expansion, and interconnect bandwidth, not model intelligence, as the candidate ceiling on progress, in the same week it asked for a verifiable pause option and Washington bolted a 30-day pre-release review onto the same models.

The walls have names you'd recognize from last week. Hardware, Hard Code, Hard Money, Hard Morality. A trillion dollars of capital is trying to bypass all four at once. It cannot. The valuations are pricing an unobstructed runway. The labs themselves are admitting there isn't one.

So here is the question I left the classroom with, and the one I would put to you. Stop benchmarking your AI strategy by what you have committed to spend. Look at what you own of the substrate. Power contracts and water rights. Transformer lead time. Magnet supply. The expertise to run any of it. The social legitimacy to keep doing so. Capital is now the cheapest input in your AI portfolio. Everything that turns it into a working asset is not. The wall is already there. The question is whether you arrived at it with anything besides money.

Olaf

On the Radar

The signals affecting the GeoTech landscape this week

Washington Buys In as the AI Labs Go Public

The state moves to take equity in the AI labs at the same moment the public market lines up to buy their shares, both arriving at the top of the cycle.

TL;DR: On June 5 President Trump confirmed the White House is exploring equity stakes in major AI companies, describing it as “almost a partnership with the American public.” The talks, first reported by the Washington outlet NOTUS, center on labs voluntarily ceding shares whose returns could fund a dividend to households. The same week, SpaceX set a single fixed IPO price of $135 a share for a roughly $1.77 trillion debut, which would be the largest listing on record by gross proceeds, and S&P Dow Jones declined to fast-track the mega-IPOs into its index. Senator Bernie Sanders countered with a bill for a 50% public stake. Anthropic says it is not in the equity talks.

BRIEFING: Two things are converging. On one side, the public market is being asked to absorb the largest equity events in its history: SpaceX at $1.77 trillion, with OpenAI and Anthropic lining up behind it, each potentially near or above $1 trillion. SpaceX broke convention by naming one fixed price before the roadshow rather than a range, a take-it-or-leave-it signal that demand is assumed rather than discovered. That confidence is doing real work, because the company reported a $4.94 billion loss in 2025 and its valuation rests heavily on AI revenue that does not yet exist at scale. When price discovery is waived at the top of a cycle, the risk does not disappear. It moves to whoever buys at the set price.

On the other side, the state is trying to buy in before the bell. The stake talks extend a pattern already visible in the administration's minority positions in Intel, MP Materials, and Lithium Americas: equity as industrial policy. What makes the AI version sharper is timing and reflexivity. A government that takes shares in a lab acquires a direct fiscal interest in that lab's valuation, which complicates its separate and growing role as the regulator of those same models. This is not a uniquely American tension. Gulf sovereign funds taking direct stakes in compute, and European states weighing public investment in their own champions, face the same conflict between owner and overseer. Sanders approaches from the opposite ideological pole and lands on a similar instrument, a 50% public stake, which is why the idea has drawn support from parts of the populist right as well. The S&P's refusal to bend its 12-month seasoning and profitability rules is the contrarian data point: the most established gatekeeper in passive investing is declining to manufacture demand on the IPOs' timeline, even as Nasdaq and FTSE Russell move the other way. The deeper question underneath all of it is who ends up holding these assets, at what price, and with what claim on the upside, at precisely the moment the labs themselves are debating whether the technology should slow down.

SO WHAT

For Executives: The IPO prices tell you about scarcity and founder leverage, not about whether your own AI spend is sound, so do not treat them as a benchmark for your own valuation or budget. The more useful read is on the labs you depend on. If you are negotiating compute, partnership, or acquisition terms with a soon-to-be-public lab, expect its cost of capital and its willingness to deal to shift the moment it lists, and lock terms before that happens.

For Policy Makers: A government equity stake and a government safety mandate point in opposite directions, and this applies to any state, not only the United States. Owning a share of a lab's upside creates a fiscal incentive to protect its valuation, which sits uneasily beside that same government's growing role as the lab's overseer. Whether you are in Washington, the Gulf, or a European capital, decide whether this trade is worth it before following the example, and if you proceed, build a firewall between the entity holding the equity and the agencies doing oversight.

For Investors: The S&P's decision is the most actionable line in the story. Passive index inclusion will lag these listings by at least a year, so the early float will be priced by retail enthusiasm and forced Nasdaq and Russell buying rather than broad institutional demand. Low float plus fixed pricing plus waived discovery is a combination that historically produces volatility in both directions. Position for the seasoning gap, not just the debut.

For Service Providers: Two distinct clients emerge. Labs approaching a listing need governance and disclosure structuring, including dual-class and controlled-company arrangements and a clear story for how a government shareholder would sit on the cap table. The investors and counterparties around them need help reading those same structures. On the communications side, a state taking equity in a private company is a narrative that can run in several directions at once, partnership, nationalization, bailout, so any lab in these talks will need disclosure language and public positioning that hold up under political scrutiny. Firms that can model the tax, control, and reputational implications of a state equity position, an unusual question a year ago, will find a narrow but well-funded engagement window.

The Brake and the Throttle: Anthropic's Pause Call Meets Trump's Cyber Order

In a single week a leading lab asks the world to consider slowing frontier AI, and Washington orders pre-release review of the same models on national security grounds.

TL;DR: On June 4 Anthropic, through its in-house Anthropic Institute, called for a coordinated, verifiable global pause option on frontier AI, warning that models are approaching recursive self-improvement, the point at which systems improve themselves without meaningful human oversight. Authors Marina Favaro and Jack Clark noted that, by the company's own account, more than 80% of code merged into Anthropic's codebase is now written by Claude. Two days earlier, on June 2, President Trump signed an executive order, Promoting Advanced Artificial Intelligence Innovation and Security, asking developers to voluntarily give the government up to 30-day pre-release access to frontier models for cybersecurity review. It is the resolution of the order Washington pulled in May.

Briefing: The two moves look opposed and are in fact the same argument from different ends. Anthropic's case rests on a claim about its own engineering: if a lab's models already write the overwhelming majority of the lab's code, by Anthropic's own reporting, and engineers ship far more code per quarter than they did a few years ago, then the loop in which AI accelerates AI is no longer hypothetical. The proposed remedy is closer to arms control than regulation. A pause is only credible if multiple well-resourced labs in multiple countries stop under the same conditions and can verify that the others have actually stopped. That verification problem, not the willingness to pause, is the hard part, and it is the part the Anthropic Institute says it will work on. The skeptical read, voiced loudly by former AI czar David Sacks, is that a lab asking government to restrain the industry days before its own IPO is positioning, not conscience.

Trump's order reads at first like a brake, a pre-release review that slows the handoff from lab to market, but its intent runs the other way, toward acceleration. The review is a checkpoint on a programme still designed to speed U.S. deployment, not to slow it. Washington nearly issued a version in May, then pulled it over fears that a longer review window would blunt U.S. competitiveness against China. The signed order cuts the window to 30 days and keeps the review voluntary. The trigger is revealing: officials moved in response to cyber capabilities that Anthropic reported in its Claude Mythos preview, which the company said could find and exploit software vulnerabilities far faster than human researchers. So the same recursive capability Anthropic frames as a control risk, Washington frames as a cyber-defense opportunity to be captured before adversaries capture it. The order routes publication costs through the Department of War and directs the prioritization of cyber defense for national security systems. The contest over who sets the terms was on open display the same week, when OpenAI published its own governance blueprint, Democratic Governance of Frontier AI. It opens from the same recursive-self-improvement premise yet pulls in a different direction, arguing that a civilian standards body should evaluate frontier models before release and that the framework should eventually be mandatory rather than voluntary, while a federal standard overrides the patchwork of state AI laws now forming. The open question is no longer whether to govern frontier models but which institution writes the rules, civilian or security, federal or state, and whose definition of the national interest prevails.

So What

For Executives: If you depend on frontier model releases for product timelines, build in the possibility that a covered model's launch slips by roughly a month for government review, and treat that as a planning input rather than a surprise. For any firm in critical infrastructure, the order's cyber-defense clearinghouse is an opening to get earlier visibility into model-discovered vulnerabilities, which can pre-empt expensive and embarrassing fixes later. Pursue that access before competitors do.

For Policy Makers: Verification is the whole game, and it is a global problem, not a national one. A pause that cannot be verified is a competitive trap that rewards whoever defects quietly, and a review window that labs can opt out of is only as strong as the incentive to opt in. The constructive path is to fund the verification and benchmarking infrastructure now, because both the pause proposal and the executive order depend on the same missing capability: the ability to confirm what a frontier model can actually do, in any jurisdiction.

For Investors: A lab publicly arguing for the option to slow its own core technology, weeks before listing, is a genuine risk-disclosure signal, not just narrative. Weigh it against the recursive-capability data the same lab is reporting. The valuations assume continued acceleration. The founders are openly pricing in the possibility of a coordinated brake. Hold both in view rather than discounting one.

For Service Providers: Demand is forming around model evaluation, red-teaming, and compliance with voluntary review frameworks. There is a parallel communications need: a lab arguing publicly for a pause, and a government framing the same capability as a defense asset, both have to manage delicate public messaging across rival audiences and governments. Firms that can operationalize the executive order's benchmarking process, help labs document capability thresholds credibly, or shape the public narrative around a pause or a security partnership are positioned for work that did not exist before June 2.

Compute Runs Dry: AI's Water Draw and the Gulf's Energy-Water Bind

The hidden input behind every AI query is freshwater, and the regions racing hardest to host compute are often the ones with the least of it.

TL;DR: Peer-reviewed work by Pengfei Li, Shaolei Ren, and colleagues at the University of California, Riverside estimates that a single 100-word AI response can consume roughly 519 milliliters of water, about a standard bottle, counting both direct cooling and the water behind the electricity. The same research line projects global AI water withdrawal of 4.2 to 6.6 billion cubic meters a year by 2027, on the order of four to six times Denmark's annual withdrawal or about half the United Kingdom's, a projection rather than a settled figure. Lawrence Berkeley National Laboratory put U.S. data center direct cooling at 17.4 billion gallons in 2023, with indirect use through the electricity those centers consume roughly twelve times larger. Much of this draw lands in already water-stressed regions, from the U.S. Southwest to the Gulf.

Briefing: Water is the input that turns AI's abstract scale into a physical limit, and the interesting part is not the per-query number but what it implies in aggregate. A bottle of water per short query is not trivial; it only looks small until it is multiplied by billions of queries a day, at which point it becomes a regional draw. That draw is concentrated in two ways that matter geopolitically. First, by source: Microsoft has disclosed that a large share of its water consumption comes from regions under water stress, and the indirect footprint, the water used to generate the electricity a data center draws, is roughly an order of magnitude larger than the water running through the cooling towers. The water question is therefore largely an energy question, and the choice between evaporative cooling and higher-energy dry cooling mostly moves the burden between two scarce resources. Second, by geography: the build-out is racing toward places with cheap power and sovereign capital but little water.

The Gulf makes the bind concrete. The UAE, Saudi Arabia, and Qatar are deploying sovereign wealth to become the largest compute hubs outside the United States, and analysts now describe compute as the new oil for economies trying to diversify away from the old kind. But cooling thousands of servers in a hot coastal climate is water-intensive in exactly the places with the least freshwater. One regional analysis puts the UAE's AI sector on track for roughly 61 billion liters of water a year by 2030, while Saudi data center power demand is projected in the same work to grow at a 29% compound annual rate, pulling water up with it; both are single-source estimates worth treating as directional. The strategic response is visible and revealing: Gulf operators are piloting next-generation cooling and pairing new campuses with solar, because renewable power consumes almost no operational water and so shrinks the indirect footprint. Most telling, Gulf states are beginning to stop treating water and electricity as limitless subsidized commodities, which is the moment a resource starts behaving like a strategic input rather than a utility. For the rest of the world, the signal is that water access, water pricing, and water disclosure are migrating from corporate-sustainability appendices into the core siting calculus for AI infrastructure.

So What

For Executives: Add water to the due-diligence checklist for any compute commitment, on the same footing as power, security, and latency. Ask prospective data center partners for direct and indirect water-use figures and the water-stress classification of the site. A campus in a drought-prone basin carries regulatory and reputational exposure that will not show up in the power bill but will surface in permitting fights, local opposition, and a broader public backlash against AI that can dampen demand and the productivity gains you are chasing.

For Policy Makers: Water is the under-regulated half of the AI infrastructure debate, and the gap is global. Power gets grid planning and permitting attention. Water rarely gets the same scrutiny at the siting stage, even though fewer than a third of operators have historically tracked it. Mandatory water-use disclosure for large data centers, tied to local water-stress data, is a low-cost intervention that lets jurisdictions price the resource before it is gone rather than after, whether the jurisdiction is in the American Southwest, the Gulf, or Northern Europe.

For Investors: Water exposure is becoming a discriminator between otherwise comparable infrastructure assets. Favor operators pairing compute with renewable power and closed-loop or dry cooling, because they carry a smaller indirect footprint and less regulatory tail risk. Conversely, evaporative cooling in a water-stressed basin is a stranded-asset risk if local authorities reprice or ration water, which the Gulf's own shift away from subsidized water suggests is coming.

For Service Providers: There is a clear opening in water auditing, cooling-system retrofit engineering, and siting analysis that integrates hydrological data. Beyond the engineering, expect demand for the communications and verification layer: water-stewardship reporting, third-party certification, and public positioning that lets an operator credibly present AI provisioning as water-conscious. Firms that can both quantify a campus's combined direct and indirect water footprint and tell that story credibly to regulators and the public will find demand from operators facing exactly the backlash described above.

The Bottleneck Is Not Money: Power, Transformers, and the Build-Out Gap

Capital is flooding into AI infrastructure faster than it can be turned into working data centers. The binding constraint is now physical, and much of it is foreign-sourced, which turns a domestic build-out into a strategic supply-chain exposure.

TL;DR: Alphabet is raising roughly $80 billion in fresh equity and has committed more than $180 billion in capital spending this year, part of more than $600 billion in combined Big Tech AI spending. Yet industry analyses find much of the U.S. data center capacity planned for the next two years is not yet under construction, and only about a third of the roughly 12 gigawatts targeted for 2026 is in active construction. The binding constraint is electrical equipment, transformers, switchgear, and grid connections, much of it sourced from China, with high-capacity transformer lead times stretching from under a year before 2020 to as long as four years now. Google's answer was to lease about 110,000 Nvidia GPUs from SpaceX for a reported $920 million a month.

Briefing: The defining feature of this moment is the disconnect between the capital and the concrete. The money has never been more available: Alphabet's first new share issuance in two decades, Amazon at $200 billion, Microsoft, Meta, and Oracle all committing at unprecedented scale. But money buys announcements, not megawatts. The bottleneck has migrated down the stack from GPUs, which were the scarce resource eighteen months ago, to the electrical gear that connects a building to the grid. Transformers and switchgear make up well under a tenth of a data center's cost, yet their order books now stretch past the entire build cycle of the facility they are meant to power. Grid interconnection queues compound the delay, and in some regions a site can wait years for a power connection. The result is the apparent contradiction at the center of the story: hyperscalers keep raising more capital even though they cannot break ground on much of what they have already announced, because the capital is a claim on future capacity in a market where the scarcest thing is a site that can actually get power on a usable timeline.

Anthropic made the same point from the inside this week. Its analysis of recursive self-improvement named chip fabrication, grid expansion, and interconnect bandwidth, not model intelligence, as a leading candidate for the binding constraint on AI progress. When the lab at the center of the boom concedes the ceiling is physical, the build-out gap stops being a logistics footnote and becomes the core strategic variable. Two implications follow, and both are geotech. The first is supply-chain dependence: a meaningful share of the transformers and components throttling the American build-out is manufactured abroad, much of it in China, which turns a domestic infrastructure story into an exposure that overlaps with the same trade tensions running through minerals and semiconductors. The second is the workaround, which is where the Google-SpaceX deal becomes a signal rather than a transaction. A hyperscaler with its own chips, its own clouds, and its own balance sheet is paying a rocket company a reported $920 million a month for access to GPUs, after Anthropic reportedly struck a similar lease at SpaceX's Colossus site for about $1.25 billion a month. When the largest infrastructure owners on earth are renting compute from a third party, the message is that owning capital and owning capacity have come apart. Google's own chief executive told investors demand is meaningfully exceeding available supply. Compute capacity, not money and increasingly not even chips, has become the scarce strategic asset, and the firms that control deliverable power and hardware now have leverage over the firms that merely have funding.

So What

For Executives: If your AI roadmap assumes capacity will be there because the spending was announced, rebuild the plan around delivery dates, not commitments. The realistic question for any compute-dependent strategy is not how much has been pledged but how many megawatts are actually energized and on what date. Secure capacity contractually now, with delivery guarantees and penalties, because the gap between announced and operational is where roadmaps quietly slip.

For Policy Makers: The constraint is grid and equipment, so that is where intervention pays off: faster interconnection approvals, transformer and switchgear manufacturing incentives, and grid expansion. There is also an industrial-security dimension worth naming, because dependence on foreign-made electrical components for domestic AI infrastructure is the same vulnerability that drives minerals and semiconductor policy, and it deserves the same attention rather than being treated as routine procurement. This is not a U.S.-only concern; every country hosting a build-out imports the same scarce gear from the same narrow set of suppliers.

For Investors: Reweight toward the physical layer. The leasing deals signal that deliverable compute, power, transformers, switchgear, and grid-tie capability is where pricing power is accumulating, while undifferentiated capital is abundant. Electrical-equipment manufacturers, independent power producers, and operators that have secured grid connections hold the scarce asset. Treat headline capex announcements as a lagging indicator and energized capacity as the leading one.

For Service Providers: Engineering, procurement, and construction firms with transformer and switchgear sourcing relationships, and consultants who can navigate interconnection queues, are positioned for sustained demand. There is also a public-affairs and communications dimension: data center build-outs increasingly hinge on local permitting, community consent, and government relations over power and land, so operators need help winning the public and regulatory argument, not just the engineering one. The most valuable near-term offering is help compressing the announced-to-operational timeline, since that gap is now the single largest risk in the build-out.

Under the Radar

The deep analysis that connects the dots

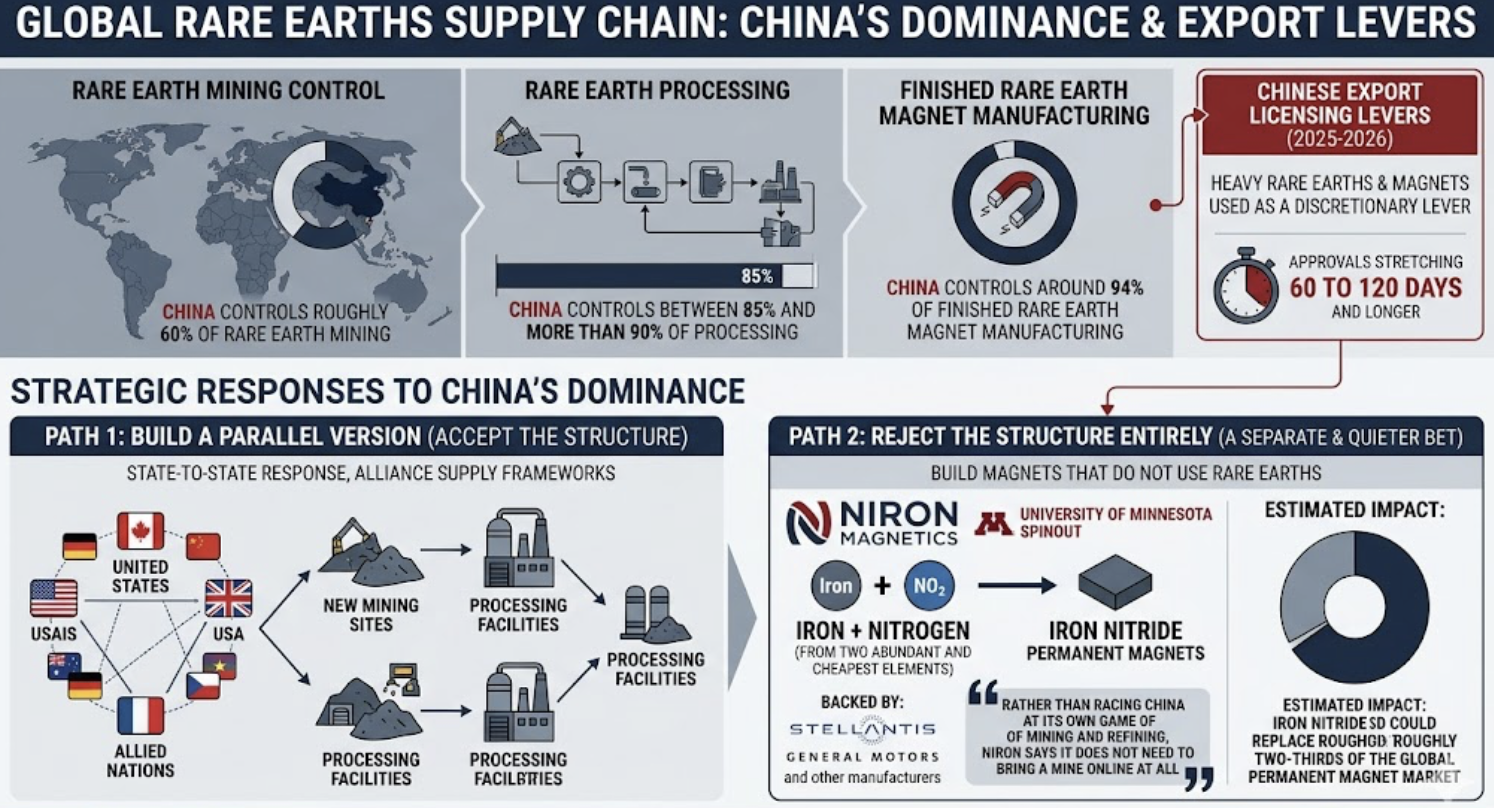

The End-Run on Beijing: Magnets Without Rare Earths

While governments negotiate supply frameworks to compete with China's processing monopoly, a cluster of firms is trying to engineer the problem out of existence, and Beijing is not standing still.

THE SIGNAL

China still controls roughly 60% of rare earth mining, an estimated 85% to 90% of processing, and around 94% of finished rare earth magnet manufacturing. As we have reported, through 2025 and into 2026 it has used export licensing on heavy rare earths and magnets as a discretionary lever, with approvals stretching 60 to 120 days and longer. The state-to-state response, alliance supply frameworks of the kind covered in prior issues, accepts the shape of the problem and tries to build a parallel version of it. A separate and quieter bet rejects that shape entirely: build magnets that do not use rare earths at all. The clearest example is Niron Magnetics, a University of Minnesota spinout commercializing iron nitride permanent magnets from iron and nitrogen, two of the most abundant and cheapest elements on earth, backed by Stellantis, General Motors, and other manufacturers. Niron's chief executive put the strategic logic bluntly: rather than racing China at its own game of mining and refining, the company says it does not need to bring a mine online at all, and estimates iron nitride could eventually replace a large share of the permanent magnet market, on the order of two-thirds by the company's own projection.

THE STAKES

The substitution bet is not a clean win, and the accurate version of the story holds three facts together. First, parallel Western capacity is real and arriving: USA Rare Earth began commercial sintered neodymium magnet production at its Stillwater, Oklahoma facility in 2026, targeting a few hundred metric tons a year and aiming toward roughly 1,200 by 2027 on its own guidance. That matters because a single advanced submarine uses several tons of rare earths and a magnet shortage has already idled auto production, so any non-Chinese supply reduces a live vulnerability. Second, the rare-earth-free path is promising but unproven at scale, and independent analysts caution that the performance data needed to verify the iron-nitride claims is not yet public. Third, and most often missed, Beijing is not a passive backdrop to any of this.

The natural question is what China does in response, and the answer is that it has several moves and is already making them. It runs its own large rare-earth-free and low-rare-earth research programs, including iron-nitride and cerium-rich magnet work, so the substitution race is not one the West is running alone. It can defend the incumbent position on price, flooding the market with cheap rare-earth magnets to undercut a young substitute before it reaches scale, a tactic it has used before in solar and other industries. It can restrict the flow of the talent, equipment, and intermediate materials that even rare-earth-free production lines still draw on. And it can move up the value chain itself, pairing its processing dominance with its own next-generation magnet research so that whichever chemistry wins, China holds a strong position. The strategic point is the divergence in approach against an incumbent that is anything but idle. Building a parallel rare earth supply chain concedes that China's vertically integrated, decades-long advantage sets the terms and tries to match it. Engineering rare earths out of the magnet concedes nothing and, if it works, makes the processing monopoly partly irrelevant rather than merely contested, but only if Western chemistries reach scale before Beijing's price and policy responses smother them. For executives and investors tracking the minerals nexus, the watch item, aside from which Western mine opens next, is whether iron nitride and similar chemistries clear independent performance verification, and how aggressively China moves to protect its position once they do. Firms exposed to magnet supply should be funding pilots and qualification testing of rare-earth-free chemistries now, treating it as a hedge whose payoff is asymmetric: modest cost if it fails, lasting relief if it works. The U.S. and allied or neutral governments should be harvesting research and intellectual property from the world's best universities to drive a rare-earth-free magnet innovation program at scale, and weighing, with clear eyes, the choice between subsidizing a parallel monopoly and subsidizing the technology that could make the monopoly moot.

Cambrian Partner By Invitation

Expert analysis from our global network

Mongolia's Hidden Strategic Asset Amid a Global Supply Chain Crisis

The global sulphur and sulphuric acid market is entering a period of acute stress. The Strait of Hormuz carries nearly half of the global seaborne sulphur trade, and military escalation has disrupted this flow at a critical moment. Prices had already surged 600%, reaching $531 per ton by January 2025 before hostilities in Iran began. Since then, prices have spiked to $600 to $800 a ton.

Sulphuric acid sits at the core of industrial value chains critical to fertilizer production, metals processing, oil refining, and chemical manufacturing. China, by using its leverage as the world's largest producer of sulphuric acid, effectively curtailing exports. While not formalized as an official blanket ban, market guidance indicates a de facto suspension of its 4.6 million annual export tonnes from May 1, prioritizing domestic fertilizer production during peak agricultural demand. Russia has adopted similar protective measures on upstream technical sulphur exports through June. The FAO warns fertilizer prices could rise 15% to 20% in the first half of this year. The fact that the world's two largest producers are choosing food security over export revenue signals how serious the shortage has become. That shift from export maximization to domestic security tightens global availability and reinforces upward pressure on industrial input costs, with second-order effects on inflation and mining economics.

What This Means for Mongolia

In the near term, some copper-producing countries, such as Mongolia, appear relatively insulated from the market pressure, and perhaps even advantaged by it. Mongolia exports most of its copper as concentrate to the Chinese market, avoiding the large domestic demand for sulphuric acid used in primary production. While Chile's acid-dependent SX-EW copper (20% of its output) and Africa's import-dependent mines face mounting pressure, Mongolia's copper output continues largely uninterrupted. The global shortage that is hurting competitors is, paradoxically, boosting Mongolia's revenues.

Copper was trading at $6.01 per pound on April 20, 2026, almost 30% higher than a year ago, and is forecast to keep rising as supply constraints from the sulphuric acid crisis tighten competitor output. Value and volume for copper exports will rise significantly in 2026. In 2025, copper exports were valued at $5.83 billion, boosting fiscal revenues.

However, Mongolia imports nearly all of its sulphuric acid, predominantly from Russia, to support limited domestic leaching operations such as Achit Ikht and Erdenet. This creates a circular dependency: Mongolia exports copper concentrate, which contains sulphur as a byproduct, yet remains structurally reliant on external suppliers for the finished sulphuric acid. As global supply tightens and prices rise, this model becomes increasingly inefficient and strategically exposed.

Recent trade data confirms early-stage repricing. Import prices for sulphuric acid into Mongolia have already trended upward into 2026, reflecting broader market dynamics. While Russia continues to supply acid, its own production constraints and export prioritization policies introduce medium-term reliability risks. A supply chain anchored to a single external partner, particularly one facing its own upstream pressures, represents a clear concentration risk.

The Inflection Point: Two Projects, One Supply Chain

The urgency lies not in current consumption, but in projected demand. The Zuuvch Ovoo uranium mine, a $1.6 billion investment agreement signed with France's Orano Group on January 17, 2025, uses in-situ leach mining, which relies on sulphuric acid as its primary extraction reagent. Mongolia's consumption is set to increase fifteen to twenty times from current levels. The investment agreement includes a planned dedicated acid plant, but securing consistent sulphur feedstock in a tightening global market remains a critical execution risk.

Longstanding plans for a new copper smelter, now in active tender with four shortlisted companies, would provide significant relief. The smelter would channel roughly 40% of the elemental sulphur it produces into a new sulphuric acid plant, yielding 988,000 tonnes of sulphuric acid per year. That is enough to supply Zuuvch Ovoo entirely, with a surplus left for export. One project's byproduct is the other's critical input. Together, their domestic supply chain may lessen Mongolia's dependency on Russia.

This alignment fundamentally changes the project economics. A decade ago, in 2016, experts calculated that only a quarter of the smelter's acid byproduct could be absorbed domestically, making the project infeasible. That constraint has now reversed, turning sulphuric acid from a byproduct liability into a strategic asset. The world is now scrambling for sulphuric acid, and for the first time Mongolia has the raw materials, the projects, and the demand to justify production at scale.

Conclusion: Strategic Timing, Not Structural Constraint

The clock is running. Zuuvch Ovoo begins production by the end of 2028, but the smelter's tender remains unresolved as of April 2026, with four international companies shortlisted and a winner yet to be selected. If construction does not begin soon, the 2028 acid demand will arrive without a domestic supply to meet it, forcing Mongolia back to expensive outside purchases. A sustained sulphuric acid supply crisis would transmit directly into mining input costs, uranium project timelines, and agricultural costs, compounding inflation already projected by the ADB to rise to 7.8% in 2026. This creates a feedback loop: commodity-driven growth would remain strong, but the inputs required to sustain that growth become increasingly constrained and expensive.

Like other resource-rich countries, Mongolia is not structurally disadvantaged. It holds the raw materials, project pipeline, and industrial logic required to build a fully integrated sulphur-to-acid value chain. The current global dislocation is not just a risk; it is a signal. As major producers prioritize domestic needs and supply chains fragment, countries with latent integration opportunities have a narrow window to reposition. The sulphuric acid war has not yet started, but for the first time, Mongolia has a real chance to win it independently of both neighbours. The raw materials exist. The demand is confirmed. The policy framework is in place. What remains is the decision to connect them before 2028 makes it urgent and the market makes it expensive.

About our partners

Zolbayar Enkhbaatar is the Founder and CEO of Capital Markets Mongolia and Think Mongol Institute. He leads international investment forums connecting Mongolia with global investors and works on issues related to economic policy, capital markets, and geopolitics. A Fulbright Scholar, he holds a Master's degree from New York University.

Ariunzaya Batgerel is a Financial Analyst at Capital Markets Mongolia, where she works on financial analysis and research on critical minerals in Mongolia. She is pursuing a BS in Finance at New York University (expected 2026) and has prior experience at Market Street Capital in New York.

About Cambrian

Cambrian Futures is a strategic foresight and advisory firm helping government, business, and technology leaders understand how emerging technologies intersect with geopolitics, markets, and national strategy. By combining rigorous research, AI-enabled analysis, and human expertise, Cambrian provides clear insight into global technology trends, risks, and power dynamics. Its work helps decision-makers anticipate disruption, manage uncertainty, and act with strategic confidence in an increasingly competitive GeoTech world.

PRODUCTION TEAM

GeoTech Radar is produced by the Cambrian Futures Insights Platform team:

CEO & Chief Analyst

Managing Director / Producer, Insights Platform

Global Lead, Smart Infrastructure Strategy

Research & Marketing Associate

Editor in Chief

Learn more about Cambrian Futures at cambrian.ai

Produced with

Human Led

Human Led +

AI Augmented

AI Led +

Human Verified

Cite as: Cambrian Futures (2026) 'GeoTech Radar Issue 23'

An important note on what this is, and is not

GeoTech Radar is directional research intended to stimulate thinking and provide geopolitical and technological context. It is not investment, legal, or financial advice, and nothing here is a recommendation to buy, sell, or hold any security or asset. The companies, valuations, and transactions discussed are described for analytical context only and serve as a backdrop to readers' own due diligence. Figures and claims are drawn from public reporting as of the publication date and may change. Readers should consult their own qualified advisers before making any decision. Cambrian Futures and the authors hold no responsibility for actions taken on the basis of this briefing.