The Intelligence Compute Gap. Brussels Locks the Cloud. Beijing Prices the Token.

IN THIS ISSUE:

CEO's Perspective

Strategic outlook from Cambrian leadership

I spent a good bit of the past week on calls with an array of experts whose knowledge will help shape a new executive course called "Frontier AI Ventures for Air, Space, Sea, and the Arctic." From Baikonur to the Bering Strait, these current and former senior government officials in the United States and Central Asia, as well as chip executives across the West, grappled with some form of the same GeoTech reality. From orbital compute to ocean autonomy, every innovator everywhere now has to bake what I call the “Four Hards” into their business model.

Hardware, Hard Code, Hard Money, Hard Morality

Each of these four authorities brings its own currency to bear. Hardware deals with chips and minerals, the physical substrate, allocated through queues and corridors. The Hard Code involves territorial laws that decide where data may sit and which providers may touch it. The Hard Money deals with a permanent price floor on frontier inference and the unwinding of cross-border deals after they have closed. And Hard Morality features a 42,300-word encyclical released into the vacuum that Washington recently created. Four Hards integrated into one inescapable stack – and none can be hedged against the others, because they are denominated in incompatible units.

That same incompatibility means the playbook every Western multinational still uses – pick a primary regulator, anchor a home jurisdiction, choose a friendly capital pool – no longer maps the terrain. Market entries now have to clear four authorities at once. Every supplier choice, every cap-table addition, and every foreign investment target must do the same. The only viable posture is governance splits inside the same company, and a level of operational ambidexterity that has no precedent. The world has never run on four polar authorities concurrently, each in its own currency. It does now. Choose to focus on just one Hard, and the other three will pick you off.

So I will ask you the questions I pondered after my calls this past week. Look at the deal you are about to sign, the supplier you are about to onboard, the market you are about to enter, the investor you are about to take money from: Can each of those decisions answer to all Four Hards at the same time? Can your organization keep them aligned when the four inevitably pull in opposite directions? If the honest answer is no, you need to rethink your strategy. You have a bet on one Hard, and the other three will not wait their turn.

Olaf

On the Radar

The signals affecting the GeoTech landscape this week

Washington's $9 Billion Intelligence AI Buildout and the Anthropic-Pentagon Split

The U.S. intelligence community cannot run frontier AI models on classified networks. A secret $9 billion budget request and a contradictory stance on Anthropic expose a deeper rift.

TL;DR: The White House approved a secret $9 billion budget request on May 22 to equip the CIA and the NSA with Nvidia Grace Blackwell superchips and the data center infrastructure to run them. The funding was reportedly necessary because U.S. spy agencies currently lack the compute to deploy frontier AI models inside classified environments. At the same time, the White House Chief of Staff authorized NSA access to Anthropic's models despite the Pentagon having designated the AI company as a supply chain risk, creating an unprecedented split in which one arm of the national security apparatus is pulling a company closer while another pushes it away.

BRIEFING: The $9 billion request targets infrastructure for Nvidia's Grace Blackwell superchip, which requires data centers with enormous electrical capacity and specialized liquid cooling. Congress must still approve the funding, but the administration is separately reprogramming $800 million for the acquisition of faster compute resources. Vinh Nguyen, former chief data scientist at the NSA and now a senior fellow at the Council on Foreign Relations, said the intelligence community needs frontier capabilities "on a timeline that matches the threat." The chip shortage has prevented agencies from testing or deploying the newest model versions on classified cloud networks.

The Anthropic dimension adds a layer of institutional contradiction. The Pentagon designated Anthropic a supply chain risk after the company refused to work on autonomous weapons systems and domestic surveillance, the first time a U.S. company has received that designation. OpenAI signed a contract with the Defense Department in Anthropic's absence. Yet White House Chief of Staff Susie Wiles separately authorized the NSA to continue using Anthropic's models, and a formal classified contract is being finalized. Unlike the Pentagon, the NSA and CIA are legally prohibited from domestic surveillance, so they can more easily accept Anthropic's guardrails.

SO WHAT

For Executives: The intelligence community's compute gap is a demand signal. Enterprises competing for Nvidia Grace Blackwell allocation should expect delivery timelines to stretch further as the federal government enters the queue with a $9 billion order. Any company building AI infrastructure on classified or regulated networks faces the same constraint the NSA faces today. Frontier models require frontier hardware, and the hardware pipeline has a single dominant supplier. Diversification planning for compute procurement is no longer optional.

For Policy Makers: The Anthropic split exposes a governance failure with implications beyond Washington. Two branches of the same national security apparatus have reached opposite conclusions about whether a U.S. AI company is trustworthy. The supply-chain-risk designation creates a precedent that could be applied to other domestic technology firms whose safety commitments conflict with military use cases. For allied policymakers in Five Eyes, NATO, Japan, and South Korea, the $9 billion Blackwell procurement compounds an existing problem: allied intelligence services depend on the same Nvidia supply chain the U.S. is now absorbing at scale. Allied governments considering Anthropic for their own classified systems must now navigate a designation that the Pentagon has applied but the NSA has overridden. Legislators on both sides of the Atlantic should examine whether a single company can simultaneously be too dangerous for one agency and essential to another, and what that means for allied interoperability.

For Investors: The $9 billion earmarked for Grace Blackwell reinforces Nvidia's dominance in the intelligence compute market, but discerning investors should ask whether the sole-source dependency is itself a risk worth hedging. AMD's Instinct MI350 series, built on CDNA 4, offers up to 288 GB of HBM3e memory per GPU, roughly 60% more than Nvidia's B200, which matters for fitting large models on fewer GPUs. AMD's MI400 line, expected to ship later in 2026 with up to 432 GB of HBM4, will target Nvidia's next-generation Rubin architecture directly. The tradeoff remains real: Nvidia's NVLink interconnect and CUDA software ecosystem are more battle-tested for large-cluster training at scale, and Blackwell systems dominated the most recent MLPerf training benchmarks. But the intelligence community's $9 billion buy creates concentration risk. Investors should price in both the Nvidia demand signal and the growing case for AMD and specialized chip alternatives as the compute buildout scales. For Anthropic, the NSA contract validates commercial demand at the highest classification levels, but the Pentagon designation constrains the total addressable government market. Defense-sector revenue will flow disproportionately to OpenAI in the near term; investors should watch for resolution of the supply-chain-risk designation as a catalyst.

For Service Providers: The classified compute buildout will require systems integrators, data center construction firms, and cooling infrastructure specialists with security clearances. The $800 million in reprogrammed funds signals immediate procurement activity before the larger congressional appropriation. Firms with existing intelligence community contracts and Nvidia partnership credentials are positioned to capture early-stage work. Clients not dedicated to defense work will nonetheless want to become proficient in dual-use dynamics of chips and models and the commensurate public attention to it.

Brussels Legislates Compute Sovereignty: Europe's Cloud and AI Development Act

The European Commission moves to restrict U.S. hyperscaler access to sensitive public-sector cloud contracts, turning digital sovereignty from aspiration into binding law.

TL;DR: The European Commission's Cloud and AI Development Act (CAIDA), the centerpiece of its Tech Sovereignty Package, would require sensitive European public-sector data to be hosted on European sovereign cloud infrastructure. AWS, Microsoft Azure, and Google Cloud collectively control roughly 70% of the European cloud market. CAIDA, expected to be finalized in early June 2026, would give European providers a meaningful procurement advantage without banning U.S. firms outright. The legislation emerges from the EU's concern that the U.S. CLOUD Act allows American authorities to compel data access regardless of where it is stored.

Briefing: Twenty-four European cloud chief executives wrote to EU Executive Vice-President for Tech Sovereignty Henna Virkkunen warning against "sovereignty washing," in which token gestures allow American hyperscalers to maintain dominance under a European label. The letter demanded reserved procurement shares for European providers, interoperability requirements, and strategic investment in domestic cloud companies. In April 2026, the Commission awarded a €180 million tender for sovereign cloud services to four European providers.

The legislation arrives at a moment when the gap between frontier AI capability and everything else is widening. SemiAnalysis estimates that Anthropic's annualized revenue grew from $9 billion at the end of 2025 to more than $44 billion by spring 2026, with inference gross margins rising from below 40% to more than 70%. A European enterprise limited to non-frontier providers risks falling behind on capability. The International Center for Law and Economics warned that CAIDA's treatment of frontier AI compute and model application programming interfaces (APIs) might matter more than any other provision, because restricting access to the only frontier compute stack that currently exists could leave European users permanently behind.

So What

For Executives: Any multinational running European public-sector contracts on AWS, Azure, or Google Cloud should begin contingency planning now. CAIDA's procurement restrictions will apply to healthcare, financial, and legal data workloads. Compliance requires more than merely moving data. It requires rebuilding application stacks on European-controlled infrastructure with materially less capability over the next three to five years. The cost of sovereignty is real for every company that does business in Europe and needs to reconfigure compute. And it will extend to their customers as it flows through to service-level agreements and customer pricing.

For Policy Makers: In light of CAIDA restrictions, the EU’s alternative path to autonomy – building domestic capacity while maintaining access to frontier AI models – requires faster data center permitting, grid expansion, and deeper capital markets. It also necessitates greatly increased funding for frontier model and/or application-specific model R&D, indigenous European startup founding, and scaling. For any international policymaker pursuing independence from U.S. and Chinese foundation models and data centers, political resolve needs to be complemented with hands-on execution programs and funding.

For Investors: European cloud providers (OVHcloud, STACKIT, Scaleway, Proximus) are the direct beneficiaries of procurement set-asides. AWS, Azure, and Google Cloud face revenue risk in the European public sector, though private-sector contracts are not currently in scope. The broader signal is regulatory fragmentation. Global cloud providers must now plan for a world in which different jurisdictions impose different sovereignty requirements on the same infrastructure. At the same time, infrastructure resilience, the ability to temporarily shift workloads between allied regional cloud providers during outages or geopolitical disruptions, requires multi-cloud architecture that most European enterprises have not yet built. Price in the risk of decreased robustness in sovereignty-first providers and premiums for those that design for cross-border failover.

For Service Providers: Cloud migration, multi-cloud architecture, and compliance consulting demand will surge in Europe. Firms that can bridge the gap between European sovereignty requirements and frontier AI access will capture the most valuable engagements. The immediate opportunity is audit and readiness assessment for public-sector clients that currently run on U.S. hyperscalers. In addition, clients will require communication plans to relay cost burdens and resilience requirements to their customers, similar to how financial institutions communicated GDPR compliance costs through updated service agreements and fee restructuring in 2018.

India-U.S. Critical Minerals Framework and the Pax Silica Architecture

A bilateral minerals deal and $20 billion Quad mobilization move the alternative supply architecture from framework agreements to industrial-scale commitment.

TL;DR: U.S. Secretary of State Marco Rubio and Indian External Affairs Minister S. Jaishankar signed the Framework on Securing of Supply in Mining and Processing of Critical Minerals and Rare Earths on May 26, alongside the existing Quad Critical Minerals Initiative targeting $20 billion in public and private mobilization. India joined the U.S.-led Pax Silica initiative in February 2026, explicitly linking critical minerals to the semiconductor and AI supply chain. India's 2026-2027 budget introduced "rare earth corridors" in four states. China still controls roughly 60% of global rare earth mining and over 90% of processing.

Briefing: The bilateral framework builds on groundwork laid at the Critical Minerals Forum in Washington in February, when India formally joined Pax Silica and signed the India-U.S. AI Opportunity Partnership. Pax Silica places critical minerals in the same strategic conversation as AI, semiconductors, and secure technology supply chains. Rubio framed the initiative in terms of vulnerability: "Vibrant innovation economies such as ours cannot afford to leave the foundational materials of these industries vulnerable to single-source monopolies that could deny us these things, not just in a time of conflict, but as a leverage point contrary to our sovereign national interests."

India's production base remains nascent. The U.S. International Trade Administration reported this year that India currently produces only four critical minerals: copper, graphite, phosphorus, and titanium. India holds an estimated 7.23 million tonnes of rare earth oxides in its monazite reserves, but limited exploration and processing capacity have constrained output. The bilateral framework addresses this gap directly: it establishes joint working groups on midstream processing technology, provides for U.S. technical assistance on rare earth separation and refining, and creates a pathway for offtake agreements that would give Indian processors guaranteed buyers. The "rare earth corridors" in India's 2026-2027 budget designate four states (Andhra Pradesh, Jharkhand, Odisha, and Kerala) for accelerated permitting, infrastructure investment, and processing facility construction. The scale of the downstream opportunity explains the urgency: McKinsey's "Wired for Growth" report projected India's electrical equipment production could rise from $50 billion to $195-235 billion by 2035, but much of that output, motors, generators, wind turbines, and EV drivetrains, depends on permanent magnets manufactured from the very rare earths India is now trying to process domestically.

So What

For Executives: The Pax Silica architecture is redefining where diversified supply chain capital should flow. Companies sourcing rare earth magnets, power electronics, or battery materials from China-dependent supply chains should evaluate India's emerging corridors as a medium-term hedge. The $20 billion Quad commitment means public co-investment is available for firms willing to anchor processing capacity in the U.S., India, Japan, and Australia. Analyze your supply chains for dependency bottlenecks and map where the India deal could provide relief in the medium to long term.

For Policy Makers: The bilateral framework is necessary but not sufficient. Although India holds the world's fifth-largest rare earth oxide reserves at an estimated 7.23 million tonnes, its midstream and downstream capacity to separate and refine the minerals does not yet exist at scale, nor does its capacity to then manufacture permanent magnets. China's advantage stems from its vertically integrated industrial ecosystem built over decades, from mining to manufacture. Pax Silica's success depends on whether allied governments can coordinate offtake agreements, fast-track permitting, and fund processing and manufacturing infrastructure simultaneously. This is a heavy lift and one that requires levels of urgency and funding similar to the Apollo space program.

For Investors: India's rare earth corridor designation and the McKinsey projection of a $235 billion electrical equipment market create a long-term investment thesis in Indian mining, processing, and power equipment manufacturing companies. The near-term risk is execution. India must expand domestic processing and manufacturing capacity roughly fivefold by 2035 to live up to Pax Silica member expectations. Companies positioned in power electronics, solar photovoltaic cells, and transformer manufacturing are the most direct beneficiaries of the policy trajectory and will be the most dependent on execution timelines.

For Service Providers: Supply chain mapping, geological survey, and processing technology consulting in India will accelerate as the rare earth corridors move from budget line to operational reality. Firms with expertise in mine-to-magnet supply chain design, environmental permitting in emerging markets, and critical minerals offtake structuring should be positioning now. Strategic dependence and public messaging on supply chain relief will need to be carefully calibrated.

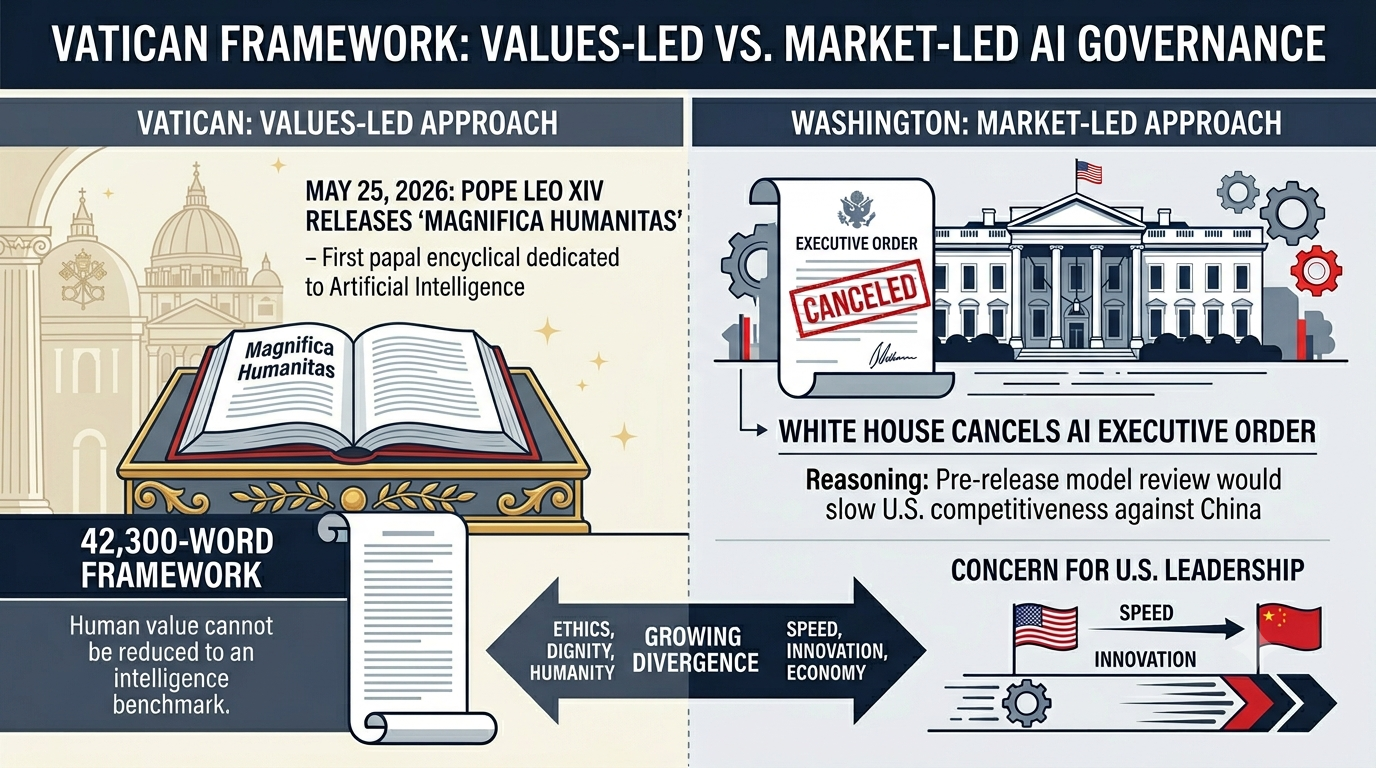

Magnifica Humanitas: The Vatican Plants a Flag on AI Governance

Pope Leo XIV's 42,300-word encyclical fills a vacuum that Washington just created, with Anthropic's co-founder presenting at the Vatican.

TL;DR: Pope Leo XIV on May 25 released Magnifica Humanitas, the first papal encyclical dedicated to AI. The 42,300-word document argues that human value cannot be reduced to an intelligence benchmark and warns that concentration of data creates "leverage over the future." Anthropic co-founder Christopher Olah presented the document alongside Leo at the Vatican. The encyclical landed between two White House reversals: on May 19, Trump scrapped an AI executive order after phone calls from David Sacks, Elon Musk, and Mark Zuckerberg. On June 2, he signed a revised version, cutting the government's model review window from 90 to 30 days and making participation voluntary. The Vatican's framework is comprehensive and values-driven; Washington's is narrow and cybersecurity-focused.

Briefing: The encyclical is not the AI doomer manifesto some expected. Pope Leo positions AI at "the beginning of the beginning" and frames his warnings as prospective – about what could happen, rather than indictments of what is happening now. The central argument is that humans, not markets and not AI systems, must remain the measure of success, reinforcing that humans have agency over and responsibility for the path of AI evolution. Paragraph 99 draws the line directly: these systems process data but "do not understand what they produce." Paragraph 178 warns that those who control the health data of entire peoples "possess a leverage over the future, for they can shape needs and markets." Leo signed the encyclical on May 15, the 135th anniversary of Leo XIII's Rerum Novarum, which addressed labor rights during industrialization and sent a clear signal of human-centricity.

The Vatican-Anthropic pairing has emerged as a lightning rod for both institutional praise and strategic critique. Anthropic co-founder Christopher Olah presented at the Vatican, operationalizing the company's commitment to widening the normative dialogue on AI's civilizational implications. This appearance coincided with Anthropic reaching a $965 billion valuation and securing NSA authorization—even as the Pentagon maintains its designation of the firm as a supply chain risk. Meanwhile, the policy terrain shifted abruptly: on May 19, President Trump scrapped his AI executive order following direct appeals from David Sacks, Elon Musk, and Mark Zuckerberg, who argued that mandatory pre-release reviews would surrender the competitive lead to Beijing. Trump framed the reversal in stark terms: "We're leading China, we're leading everybody, and I don't want to do anything that gets in the way." By June 2, the administration pivot resulted in a revised order establishing a voluntary framework for model testing with truncated 30-day review windows. The new order explicitly rejects mandatory licensing, reducing federal oversight to a request rather than a requirement. In contrast, the Vatican's framework is neither narrow nor voluntary; it stands as the most comprehensive governance architecture yet articulated, centering human dignity across the entire stack of labor, data concentration, and autonomous systems.

So What

For Executives: The encyclical will not create binding regulation, but it will influence the normative environment in which regulation is shaped. Leo's framing of data concentration as leverage over the future is directly relevant to any company that aggregates health, financial, or behavioral data at population scale. In markets where Catholic social teaching influences policy, particularly parts of the U.S., Latin America, Southern Europe, the Philippines, and parts of Africa, expect the encyclical to be cited in legislative debates over data governance and AI labor protections. In your AI governance, product designs, market postures and communications, embrace those customer segments and their need for solutions that respect human dignity.

For Policy Makers: When the world's most powerful government explicitly refuses to regulate AI and the world's oldest governance institution steps into the vacuum, that is a signal about where normative authority over frontier technology is migrating. The contrast between Washington's canceled executive order and the Vatican's 42,300-word framework reflects a growing divergence between geopolitical and market-led approaches on one side and values-led approaches on the other. The EU's AI Act, the Vatican's encyclical, China’s state-stability control of AI, and the absence of U.S. federal AI legislation now form a four-way landscape that policy makers in every jurisdiction must navigate.

For Investors: Companies that the Vatican's framework would flag, e.g. those concentrating data, displacing labor without mitigation, or deploying autonomous decision systems without human oversight, will face growing customer scrutiny and pressure in jurisdictions where the encyclical carries weight. Last week's GeoTech Radar coverage of Gen Z workplace sentiment data illustrated how generational skepticism toward AI translates into tangible brand and talent risks for portfolio companies. But there is a harder economic side, too. A San Francisco Federal Reserve brief published on May 27 found that individual workers are becoming more productive with AI, but economy-wide total factor productivity has not moved, echoing the 1990s internet paradox. The gap between micro-level adoption and macro-level measurement means the labor displacement Leo warns about could arrive before the productivity gains that are supposed to offset it. Price this lumpy productivity and customer acceptance picture into your asset pricing.

For Service Providers: The encyclical creates demand for ethical AI advisory, governance framework design, and stakeholder engagement services, particularly for multinational clients operating in Catholic-majority markets. Consider also the Pope’s moral authority and signalling might carry beyond Catholic or even Christian communities. Firms that can translate the encyclical's principles into auditable governance metrics will be positioned for a new category of compliance work and garner greater levels of trust among customer segments that remain skeptical of AI progress.

Under the Radar

The deep analysis that connects the dots

Beijing Prices the Token, Locks the Door

China commoditizes frontier AI inference while ordering the reversal of Meta’s $2 billion cross-border acquisition of Manus. Two mechanisms, one strategy.

The Token Commodity

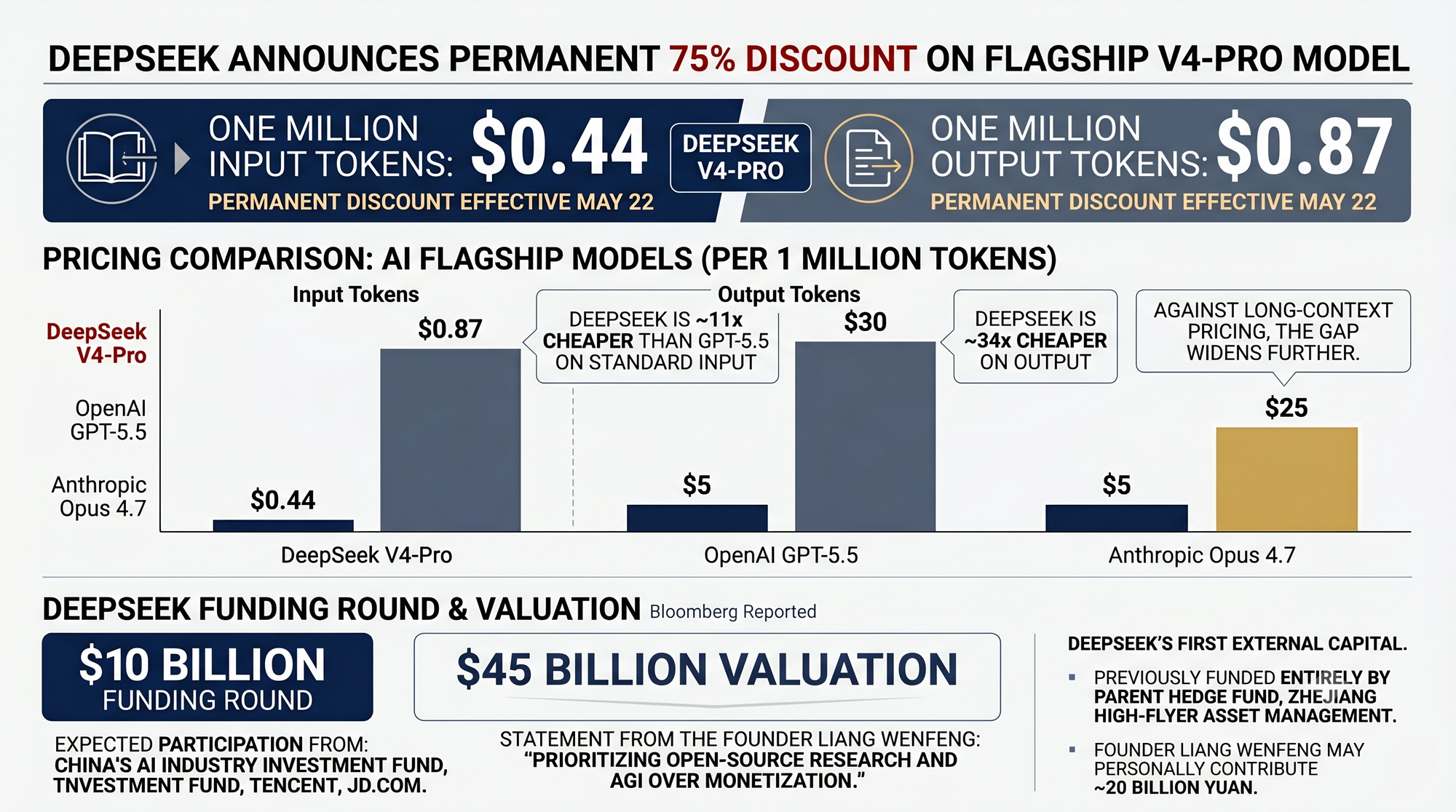

DeepSeek announced on May 22 that its 75% discount on its flagship V4-Pro model would become permanent. One million input tokens now cost $0.44. One million output tokens cost $0.87. That makes DeepSeek roughly 11 times cheaper than OpenAI's GPT-5.5 and Anthropic's Opus 4.7 on input tokens (both at $5 per million) and as much as 34 times cheaper on output tokens ($30 per million for OpenAI and $25 per million for Anthropic). Against long-context pricing, the gap widens even further.

The pricing decision arrived alongside a funding milestone. Bloomberg reported that DeepSeek is closing a $10 billion funding round at a $45 billion valuation, with expected participation from China's AI Industry Investment Fund, Tencent, and JD.com. Founder Liang Wenfeng told investors the company will prioritize open-source research and artificial general intelligence (AGI) over monetization. This is DeepSeek's first external capital, the company having been previously funded entirely by its parent, the hedge fund Zhejiang High-Flyer Asset Management. Liang could personally contribute roughly 20 billion yuan to the round.

The strategic logic is not commercial, at least not in the Western sense. DeepSeek is pricing to set a floor under the global cost of frontier inference, not maximize revenue. As Bloomberg analysts have described it, Asia is treating AI tokens as tradable industrial commodities rather than premium software. It is not coincidental that DeepSeek, which closely matches Anthropic's capability, made frontier-class inference permanently cheap during the same week that Anthropic crossed into profitability for the first time at $47 billion annualized revenue and a $965 billion valuation. Two AI economies are forming with incompatible pricing logic and different relationships between state capital and model development. The valuation gap itself tells the story: Anthropic's $965 billion reflects a market that prices AI labs on revenue trajectory and IPO potential; DeepSeek's $45 billion reflects a system that prices them on strategic utility to the state. The gap is not a market inefficiency. It is two different theories of value.

The Ownership Firewall

The pricing architecture tells one half of the story. The ownership architecture tells the other. On April 27, China's National Development and Reform Commission (NDRC) formally ordered the unwinding of Meta's $2 billion acquisition of Manus, the Chinese-founded AI agent company that had relocated to Singapore and restructured ownership before the sale. The deal had closed in December 2025. The money exchanged hands. Roughly 100 Manus employees had moved into Meta's Singapore offices. Beijing ordered the deal’s reversal anyway.

On May 21, Bloomberg reported that Manus's three co-founders are in talks to raise roughly $1 billion from external investors to buy the company back at a valuation matching or exceeding the original $2 billion. The founders might contribute personal capital to close the gap. The buyback would restructure Manus as a China-linked joint venture with a possible Hong Kong listing path. GTR covered Beijing's investigation of the acquisition in Issue 16, when the case was about extraterritorial assertion. The story now is about forced reversal as a sovereign instrument that drives the decoupling of the two AI Economy models described above. A blocked acquisition is a familiar tool of statecraft, but an unwound acquisition, one that had already closed, with capital deployed and employees integrated, is a new category of action. The bridge between AI economy models gets torn down because of fears that one model could dominate the other.

Read these two developments together and the pattern is clear. Beijing is building a parallel AI economy with two reinforcing mechanisms that distinguish it from the U.S. model. The first is pricing – make frontier inference so cheap that the global market has no economic reason to consolidate around Western providers. The price-sensitive Global South will reward this. The second is ownership – ensure that Chinese-origin AI technology, no matter where it relocates or who acquires it, remains within the Chinese AI economy model. The combination creates a system in which China's AI ecosystem can compete globally on cost at near-parity performance levels, while both China and the U.S. remain closed to reciprocal ownership. For executives and investors tracking the AI supply chain, the question is no longer whether bifurcation is happening. It is whether your portfolio, your procurement, and your partnerships are priced for two separate AI economies with two separate economic and geopolitical logics and rule sets.

About Cambrian

Cambrian Futures is a strategic foresight and advisory firm helping government, business, and technology leaders understand how emerging technologies intersect with geopolitics, markets, and national strategy. By combining rigorous research, AI-enabled analysis, and human expertise, Cambrian provides clear insight into global technology trends, risks, and power dynamics. Its work helps decision-makers anticipate disruption, manage uncertainty, and act with strategic confidence in an increasingly competitive GeoTech world.

PRODUCTION TEAM

GeoTech Radar is produced by the Cambrian Futures Insights Platform team:

CEO & Chief Analyst

Managing Director / Producer, Insights Platform

Global Lead, Smart Infrastructure Strategy

Research & Marketing Associate

Editor in Chief

Learn more about Cambrian Futures at cambrian.ai

Produced with

Human Led

Human Led +

AI Augmented

AI Led +

Human Verified

Cite as: Cambrian Futures (2026) 'GeoTech Radar Issue 22'

An important note on what this is, and is not

GeoTech Radar is directional research intended to stimulate thinking and provide geopolitical and technological context. It is not investment, legal, or financial advice, and nothing here is a recommendation to buy, sell, or hold any security or asset. The companies, valuations, and transactions discussed are described for analytical context only and serve as a backdrop to readers' own due diligence. Figures and claims are drawn from public reporting as of the publication date and may change. Readers should consult their own qualified advisers before making any decision. Cambrian Futures and the authors hold no responsibility for actions taken on the basis of this briefing.