The Beijing Tech Bargain. Foundry Diplomacy. The Indium Leverage.

IN THIS ISSUE:

CEO's Perspective

Strategic outlook from Cambrian leadership

As leaders, we yearn for deals that resolve global tensions and relieve pressure – and sometimes we skim past the fine print in our anticipation for them. The fine print is where the deal actually sits.

Look at the agenda Trump and Xi will work through in Beijing on Thursday and Friday. Then look at what is missing from it – semiconductors, frontier AI, rare earth magnets, and nuclear stability. The summit will produce real deliverables on agriculture, aircraft, and a new Board of Trade, but the questions that truly drive the countries’ relationship will not be in the room.

The carve-out is the real deal

This week’s headlines describe some crucial agreements, including the Trump-Xi summit, the Apple-Intel foundry deal, the White House model vetting framework, and Anthropic's Akamai contract. But the agreements are not what matters most. The bigger story is what the various parties left outside the agreements.

China removed indium from the November truce, making it the only mineral excluded when gallium, germanium, and antimony were paused. These minerals are used in every touchscreen, LCD, OLED display, CPUs and GPUs, chargers for laptops and phones, power electronics in EVs and 5G equipment, fibre-optic cables, and in thin-film photovoltaics. China produces and refines the overwhelming majority of all four — roughly 98% of gallium, ~68% of germanium and indium, and ~48% of mined antimony (but 70–90% of refined antimony) — while the United States produces essentially none of any of them and imports nearly 100% of its needs, mostly from China directly or via Chinese-refined supply routed through Korea, Belgium, and Southeast Asia. Apple is carving foundry capacity out of its TSMC dependency, not because TSMC has failed but because single-supplier exposure to a single jurisdiction has become a board-level risk that can no longer sit on the balance sheet quietly. The White House is preparing to carve frontier AI models out of the general software regulatory regime and place them inside a pre-release vetting process modeled on FDA approval. Anthropic is carving compute capacity out of the hyperscaler oligopoly through Akamai and SpaceX, and as the largest demand-side buyer of frontier compute, it is setting precedents that smaller buyers will follow.

This is where last week's argument extends. Last week I wrote about institutions strained past their design. The carve-out is one of the cleanest mechanisms by which that straining happens, and not always for ill. You do not need to break a framework to weaken it, and you do not need to break it to make room for evolution either. You only need to define carefully what it does not cover, and to put the items that actually matter in the excluded category. The framework keeps its name and its standing. Its scope quietly contracts or shifts. The negotiating attention moves to the boundary, not the contents. The deal that matters most becomes the list of exceptions.

These decisions cut both ways. China's indium carve-out is leverage held in reserve. Apple's Intel carve-out is a hedge against a concentration risk that should never have been allowed to build up in the first place. The same mechanism can be predatory or constructive depending on who is wielding it and what they are reserving from the room. The discipline is reading the move accurately, not assuming it is always one or the other.

The work this week is to read every framework you depend on through its exclusions rather than its inclusions. Which of your supplier agreements, regulatory regimes, alliance commitments, or trade frameworks has a list of exceptions that has grown longer, or more strategically significant, in the past 18 months? That list, not the framework around it, is where your real exposure sits, and where someone else's real intent is being signaled. Most boards do not track it that way. The ones that start to do so will race ahead of those still reading the press release.

Olaf

On the Radar

The signals affecting the GeoTech landscape this week

The Beijing Tech Bargain

Trump and Xi will sit down on Thursday and Friday to manage the relationship, not reform it. Semiconductors, artificial intelligence model exports, and rare earth minerals stay outside the room.

BRIEFING: On Thursday and Friday, President Trump will meet President Xi Jinping in Beijing for the first sitting United States presidential visit to China in nearly ten years. Brookings, the Council on Foreign Relations, and the Wire China all expect a similar set of deliverables, including a Chinese commitment to purchase roughly 30 billion dollars in United States agricultural goods and Boeing aircraft, and the announcement of a new "Board of Trade" mechanism that would identify non-strategic sectors where managed trade can proceed alongside continued export controls on advanced technology. Trump took chief executives from Nvidia, Apple, Tesla, Exxon, Boeing, Qualcomm, Blackstone, Citigroup, and Visa, including Jensen Huang, Tim Cook, and Elon Musk, with him on the trip.

What is not on the agenda is more telling than what is. The two governments have agreed to defer the questions that actually drive the relationship. China's flooding of third-country markets with subsidized electric vehicles, steel, solar panels, and batteries continues, with a goods trade surplus on track to clear 1.2 trillion dollars again this year. Beijing's nuclear buildup toward 1,500 warheads by 2035 has no arms control framework. The practice of Chinese laboratories training cheaper models on the outputs of frontier United States models, including DeepSeek's V4 release in April that pairs Nvidia processors with Huawei chips, has no governance mechanism. DeepSeek itself just opened its first external fundraising at a 50 billion dollar valuation, with China's 8.8 billion dollar national artificial intelligence fund lined up as lead investor and Tencent in participation talks. Beijing is institutionalizing its artificial intelligence champions while the summit defers the question of how the two sides will compete on the technology itself.

SO WHAT

For Executives: Treat the summit as a stability event, not a settlement event. The Board of Trade will likely produce sector-by-sector tariff adjustments and purchase commitments that change the cost calculus on agricultural inputs, commercial aircraft, and selected manufactured goods, but it will not change the trajectory on advanced semiconductors, AI model exports, or critical minerals. If your business depends on stable access to either Chinese demand or Chinese supply in those three categories, plan for continued volatility. Map your exposure into strategic and non-strategic buckets now, and brief your board on which side of that line each product sits on. The companies that emerge strongest from the next 18 months will be the ones that have priced in the carve-out, not the ones counting on it to close.

For Policy Makers: The summit institutionalizes a managed-competition framework that resembles the U.S.-Japan trade talks of the early 1990s more than any prior U.S.-China engagement. That framework was eventually abandoned as ineffective. Watch for whether the Board of Trade includes a dispute resolution mechanism that gives both sides an off-ramp before tariff escalations. Without one, the pattern of episodic crises will resume after the November midterms. The harder issue is what the framework leaves unaddressed. here is currently no crisis communications channel between the two countries for artificial intelligence incidents, no successor to the New Strategic Arms Reduction Treaty for nuclear stability, and no agreement on the training of Chinese models on frontier United States outputs. A summit that produces a Board of Trade without parallel structures for those three issues kicks the can down the road.

For Investors: The market will price the summit as a de-escalation, with rotation into companies exposed to Chinese demand and consumer sectors. Resist that read on the strategic technology stack. Anthropic's reported $900 billion pre-money valuation, DeepSeek's $50 billion round with state-backed lead investors, and Akamai's $1.8 billion Anthropic deal all signal that the AI capital expenditure cycle is intensifying on both sides of the relationship, regardless of the summit. Position around the technology decoupling that the summit explicitly preserves, such as domestic semiconductor manufacturing, rare earth processing outside China, and Western AI infrastructure providers that operate outside the Chinese market entirely. Selectively, Boeing and the U.S. agricultural complex are the cleanest summit beneficiaries on a six-month view.

For Service Providers: Clients will read the summit headlines as a signal that the relationship is stabilizing. The communications work is to keep them focused on what the summit does not change. For European multinationals, the Board of Trade does not affect their exposure to Chinese overcapacity flooding their domestic markets. For U.S. clients with Chinese supply chain dependencies in the strategic categories, the summit changes nothing about export control trajectories or the political risk of a post-midterm policy snapback. Brief clients on the difference between the commercial deliverables that will dominate coverage and the strategic conditions that remain unchanged. The post-midterm window is when a clear-eyed framework, prepared now, will be most valuable.

Foundry Diplomacy

Apple breaks its sole-supplier reliance on Taiwan Semiconductor Manufacturing Company (TSMC). Intel becomes a national security utility. The chip supply chain rearranges ahead of the summit.

Briefing: On May 8, the Wall Street Journal reported that Apple and Intel reached a preliminary agreement for Intel to manufacture some Apple-designed chips. Intel shares jumped roughly 14 percent on the news. The agreement does not return Intel-designed central processing units to Macs. Instead, Intel acts as a contract foundry, fabricating chips that Apple still designs internally. For Apple, the deal ends a five-year period of sole reliance on Taiwan Semiconductor Manufacturing Company since the 2020 transition to Apple Silicon. For Intel, it is the most consequential validation yet of a foundry business that many analysts had expected to be abandoned or spun off.

The Apple agreement joins an Intel foundry customer base built rapidly under chief executive Lip-Bu Tan, who took over in spring 2025. Microsoft signed a foundry deal for Intel's 18A process in February 2024 for custom chips, Amazon Web Services followed in September 2024 with a multi-year, multi-billion-dollar foundry agreement covering custom artificial intelligence fabric chips, the United States government committed 3 billion dollars in exchange for military-purpose semiconductor production, and Elon Musk announced last month that his planned 119 billion dollar Terafab in Austin will rely on Intel's future 14A node. Intel's foundry division is now expected to break even in 2027. Separately, on May 8, Bloomberg reported that the United States is investigating Bangkok-based OBON Corporation, a firm linked to Thailand's national artificial intelligence initiative, for allegedly routing 2.5 billion dollars in Super Micro Computer servers containing advanced Nvidia chips to Chinese customers including Alibaba between 2024 and 2025. The diversion case underscores why foundry diversification has become national security policy rather than corporate strategy.

So What

For Executives: Single-supplier dependency on TSMC has been the unspoken assumption underwriting most enterprise hardware roadmaps for the past five years. That assumption is now actively being revised by the largest buyers in the market, including the company that pioneered the Taiwan-only model. If your hardware roadmap, your data center buildout, or your product launch schedule assumes a single foundry, treat the Apple-Intel deal as a forward signal that your peers could be quietly diversifying. Sourcing teams should engage Intel Foundry, Samsung Foundry in Texas, and select mature-node alternatives in parallel to existing relationships. The premium for second-source qualification will fall as Intel ramps. The penalty for waiting will rise.

For Policy Makers: The Apple-Intel deal validates the central premise of the 2022 Creating Helpful Incentives to Produce Semiconductors Act and the United States government's direct equity stake in Intel, bolstering the belief that subsidies and procurement commitments could rebuild a domestic foundry base capable of competing with Taiwan. The harder questions are whether Intel can execute with the same reliability as Taiwan Semiconductor Manufacturing Company and whether the model is replicable beyond Intel. Samsung has run mature-node fabs in Austin for nearly two decades, but its leading-edge plant in Taylor, Texas has slipped mass production into 2027, and no other domestic player is on the horizon. The next phase of policy work is end-use verification at allied transit points, drawing directly on the OBON Corporation case, and a hard look at whether the United States needs additional leading-edge foundry capacity beyond Intel and Samsung to credibly survive a Taiwan contingency. The summit conversation in Beijing will not address this. The domestic conversation must.

For Investors: Intel has gone from one of the worst performers in the S&P 500 to one of the best on a year-to-date basis, with shares up more than 200%. The Apple deal extends that runway, but the operational risks remain real. Its 14A volume production is not expected until 2029, and Apple has not disclosed which products will use Intel-fabricated chips. Pair Intel exposure with the foundry equipment ecosystem, particularly companies with diversified customer bases across Intel, Samsung, and TSMC. Apple itself is less affected on a one-year view, but the deal de-risks its long-term supply story. The clearest losers are pure-play TSMC suppliers and any company in the chip value chain whose thesis depends on continued Apple-TSMC exclusivity.

For Service Providers: Foundry diversification is now a board-level conversation for any client with a hardware roadmap, a data center program, or a regulated supply chain disclosure obligation. The communications work is to translate the Apple-Intel signal into a client-specific question. Where is our single-source semiconductor exposure, and what is our diversification timeline? For European clients, layer in the European Chips Act trajectory and the political economy of subsidies. For Asia-Pacific clients excluding Taiwan, focus on the Samsung Texas timeline and the dual-foundry strategies that the largest U.S. customers are now adopting.

The Sovereign Model Gate

The White House drafts pre-release vetting for frontier models. The transatlantic regulatory map redraws. Anthropic's Mythos becomes the precedent.

Briefing: On May 4, the New York Times reported that the White House is considering an executive order to create a working group of government officials and industry leaders to vet new artificial intelligence models before public release. National Economic Council Director Kevin Hassett confirmed the direction on Fox Business on May 6, comparing the proposed framework to Food and Drug Administration approval for new drugs. The framing is not new. In a 2019 Wired piece, Cambrian Futures chief executive Olaf Groth wrote with Mark Nitzberg and Stuart Russell that artificial intelligence algorithms need Food and Drug Administration-style drug trials before deployment to the public. The argument was ahead of its time. It is now the working assumption inside the West Wing. The Commerce Department on May 5 announced that Microsoft, Google, and xAI had agreed to join the voluntary pre-release testing program operated by the Center for Artificial Intelligence Standards and Innovation, putting all five United States frontier laboratories inside the same framework. President Trump told the Consumer News and Business Channel last week that United States officials had "very good talks" with Anthropic, signaling a thaw after months of public conflict.

The catalyst is Anthropic's Mythos model, which the company has held back from public release because it can identify thousands of software vulnerabilities in seconds. The National Security Agency has reportedly used Mythos to assess vulnerabilities in government software, even while the formal Defense Department procurement of Anthropic remains under litigation. Mozilla credited Mythos with helping ship 423 Firefox security fixes in April alone, compared to 31 a year earlier. The European Commission has separately been in dialogue with Anthropic about bank vulnerability testing. The architecture taking shape is closer to the United Kingdom's Artificial Intelligence Security Institute, which operates pre-deployment evaluation programs with formal access agreements covering Anthropic, OpenAI, Google DeepMind, and Meta, than to the Biden-era executive order Trump revoked on taking office. A United States working group of the kind the New York Times article describes would not match the Artificial Intelligence Security Institute's depth on day one, but it would establish the counterpart that has been notably absent from the post-Biden landscape.

So What

For Executives: If you are deploying frontier AI in regulated industries or in customer-facing products, the question is no longer whether your model provider has been government-vetted, but how that vetting changes your liability picture, your procurement posture, and your enterprise risk register. Update your vendor risk frameworks to track which models are inside the Center for Artificial Intelligence Standards and Innovation program and what the testing covers. Brief your audit committee on the trajectory – from voluntary participation today, to formal executive order vetting in the coming months, to potential statutory requirements after the midterms. Companies that wait for the rules to crystallize will be playing catch-up against peers that have already mapped their model dependencies to the emerging regulatory taxonomy.

For Policy Makers: The proposed working group is the first material step back toward systematic federal AI oversight under this administration, and it puts the U.S. on a convergence path with the United Kingdom and a partial alignment with the European Union Artificial Intelligence Act framework. That convergence has both costs and benefits. It reduces the transatlantic compliance burden for frontier laboratories and creates a shared evaluation base for safety research. It also concentrates the gating authority in a small number of government bodies that will face intense lobbying and capacity constraints. The implementation question is whether the working group will have testing capacity proportional to the release cadence of frontier models, which is now measured in weeks. Without dedicating resources to the testing infrastructure at a similar rate, the executive order risks becoming a paper requirement.

For Investors: Pre-release vetting is structurally favorable to incumbent frontier laboratories with the resources to participate in voluntary programs and the regulatory affairs teams to navigate formal review. It is structurally unfavorable to second-tier laboratories and open-weight projects that lack the institutional capacity for the same engagement. Expect the regulatory framework to harden the moat around OpenAI, Anthropic, Google DeepMind, Microsoft, and xAI. For Chinese open-weight models, including DeepSeek's V4 and the Alibaba Qwen family, the vetting framework creates an additional barrier to U.S. enterprise adoption that exists alongside the existing export control regime. Watch for whether the executive order extends to import controls on foreign-trained models deployed in U.S. enterprises, which would be the policy equivalent of the chip export control regime applied to AI weights.

For Service Providers: This is one of the cleanest client communications opportunities of the second quarter. Every client deploying AI at scale will face questions from boards, regulators, and counsel about how the proposed vetting framework affects their model selection, their disclosure obligations, and their crisis preparedness if a vetted model is later found to have a vulnerability. Build a one-page client briefing that covers the Center for Artificial Intelligence Standards and Innovation participants, the Mythos precedent, the United Kingdom Artificial Intelligence Security Institute parallel, and the European Union dimension. For European clients, layer in the European Union Artificial Intelligence Act compliance overlap. For pharmaceutical and financial services clients, draw the explicit analogy to existing pre-release approval frameworks, which is exactly the framing the Trump administration has chosen to use.

The Compute Multipolarity

Anthropic's Akamai and SpaceX deals could end the U.S. hyperscaler oligopoly. The Children's Investment Fund's exit from Microsoft is the investor signal.

Briefing: On May 7 and 8, Anthropic signed a 1.8 billion dollar, seven-year cloud computing agreement with Akamai Technologies, the largest contract in Akamai's 28-year history. Akamai, founded in 1998 out of research at the Massachusetts Institute of Technology, operates a globally distributed network of edge servers in dozens of countries, originally built to accelerate web content delivery and now repurposed for low-latency artificial intelligence inference. Akamai stock rose 27 percent on the disclosure. The deal landed days after Anthropic announced it would access compute capacity on Elon Musk's SpaceX-operated cluster of 220,000 Nvidia graphics processing units, which had previously powered xAI training runs. Anthropic chief executive Dario Amodei said at the company's developer conference that Anthropic saw 80 times growth in annualized revenue and usage during the first quarter, driving urgent demand for additional compute capacity beyond what Google Cloud and Amazon Web Services could provide on the timeline required. Anthropic is on track to spend an estimated 80 to 100 billion dollars across cloud providers through 2029.

The same week, the Children's Investment Fund disclosed it had cut its Microsoft position from 10 percent of its portfolio at the end of 2025 to just 1 percent by the end of March 2026, exiting roughly 8 billion dollars of stock. Founder Christopher Hohn cited artificial intelligence disruption risk to Microsoft's Office productivity franchise and growing competitive pressure on Azure, where Google Cloud's 63 percent year-over-year growth has begun to overshadow Azure's 40 percent. Duquesne Family Office and Tiger Global made similar reductions. Cloudflare announced layoffs of 1,100 workers the same week, framing the cut as a transition to an agentic artificial intelligence-first operating model. The artificial intelligence compute layer is no longer a stable oligopoly of three United States hyperscalers. It is becoming a multipolar map of hyperscalers, edge networks, sovereign clouds, and merchant providers, with Anthropic acting as the single largest demand-side catalyst.

So What

For Executives: If your enterprise AI strategy is built on the assumption that compute will be procured through a hyperscaler relationship, that assumption is now an open question rather than a fixed input. The Anthropic-Akamai deal proves that frontier laboratories will reach for any provider capable of delivering low-latency inference at scale, including content delivery networks that no one categorized as cloud infrastructure two years ago. Re-examine your vendor mix. Identify whether your latency-sensitive workloads could be served by edge networks rather than centralized cloud regions. Negotiate sovereign data residency commitments where regulations require them. The leverage on compute pricing has shifted toward buyers for the first time since 2022.

For Policy Makers: The fragmentation of the AI compute base is a national competitiveness opportunity. For U.S. policy, it argues for explicit support of edge network and merchant compute providers, who can offer geographic and counterparty diversification that pure-play hyperscaler concentration cannot. For European Union and United Kingdom policy makers, the Anthropic-Akamai deal is a template for sovereign compute strategies that do not require building hyperscalers from scratch. Akamai operates one of the world's largest distributed edge platforms, with regulatory profiles already negotiated in dozens of jurisdictions. The policy work is to ensure that domestic data residency, security clearance, and procurement frameworks accommodate this multipolar map rather than continue to assume the three-hyperscaler default.

For Investors: The Children's Investment Fund's Microsoft exit is the most significant repositioning by a top-tier hedge fund in AI in 18 months. Read it as a directional signal, not a liquidation. The fund rotated from Microsoft into Alphabet, increasing its Alphabet stake from 3 % to 5%. The thesis is that Microsoft's Office franchise faces real disruption from AI-native productivity tools, including Anthropic's general availability inside Word, Excel, and PowerPoint announced the same day. Rebalance accordingly. Akamai is now an AI infrastructure story, not a content delivery network story. The merchant GPU ecosystem, including Coreweave, Crusoe, and Lambda, is the second-derivative play. The contrarian position is selectively long Microsoft on the assumption that Copilot eventually monetizes, but the consensus is moving the other way.

For Service Providers: Clients are about to ask why their cloud strategy looks nothing like Anthropic's. The honest answer in most cases is that it should not, because most enterprises are not training frontier models. The communications work is to translate the Anthropic-Akamai signal into the relevant client question. What does multipolarity in compute mean for our regulatory posture, our data residency, our latency requirements, and our vendor concentration risk? For European clients with sovereign cloud mandates, the answer is increasingly yes, you should be looking at non-hyperscaler options. For U.S. enterprises in regulated industries, the answer is selectively, with focus on edge inference and on geographic redundancy. Avoid the trap of treating the Anthropic-Akamai deal as a generalized recommendation. It is a market-structure signal, not a one-size-fits-all procurement template.

Under the Radar

The deep analysis that connects the dots

The Indium Leverage

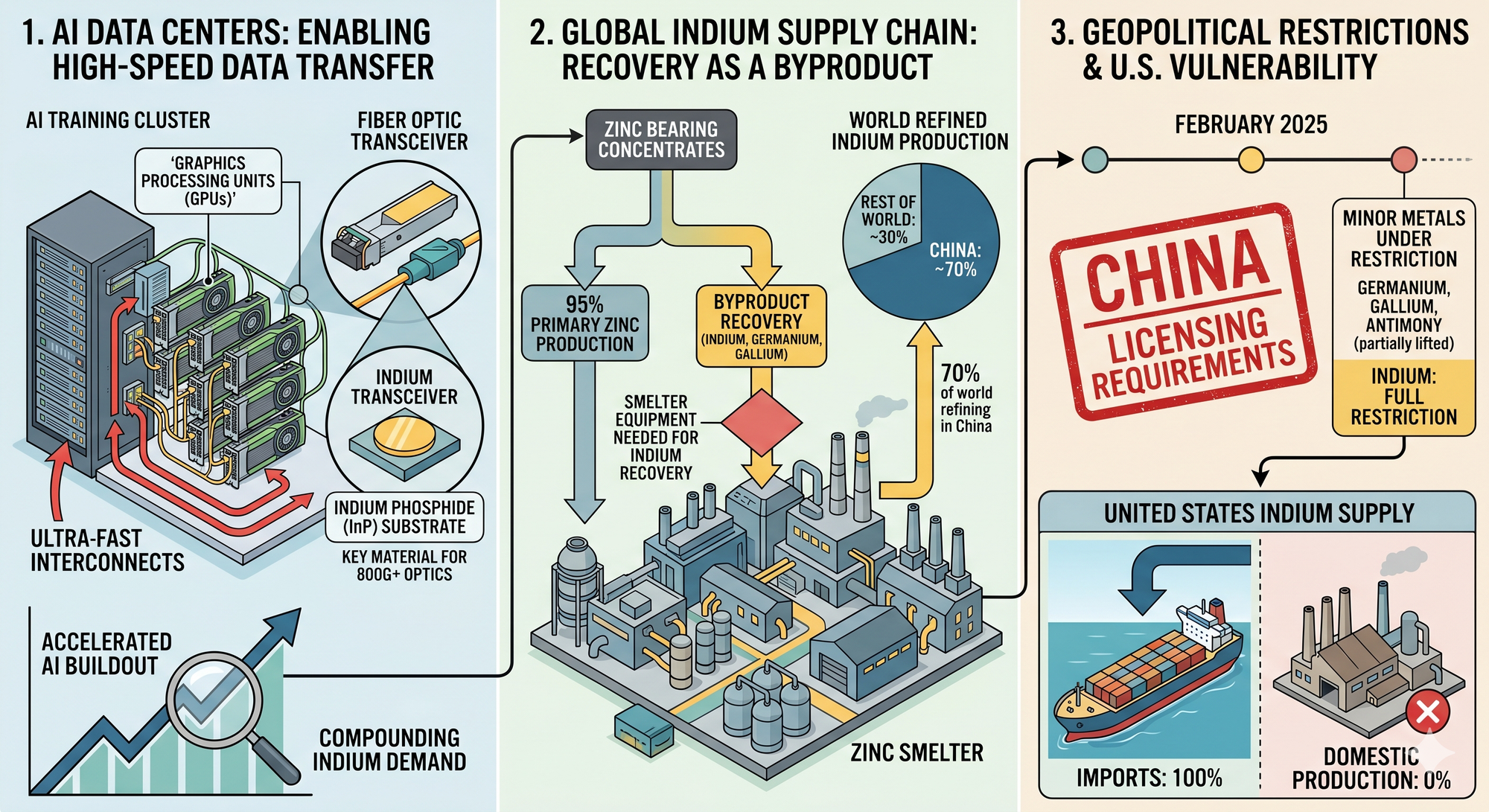

The single critical mineral that survived the November 2025 United States-China trade truce, which paused export controls on gallium, germanium, and antimony but left indium under full restriction, now constrains every artificial intelligence data center buildout. China holds 70 percent of refined supply. The United States produces none. Hardly anyone is talking about it.

The Material That Powers Every AI Data Center

Every artificial intelligence data center built in the past two years relies on indium phosphide substrates to send data between graphics processing units through fiber optic cables. No other material can do this job at scale. Indium gallium arsenide compounds extend the use case into high-speed data networks and emerging applications in 5G infrastructure and copper indium gallium selenide thin-film solar. As the buildout of artificial intelligence training and inference clusters accelerates, the demand for indium has compounded with it. The United States Geological Survey 2025 indium summary notes that demand from data center optics and renewable energy infrastructure now drives the marginal price.

The Carve-Out That Tells the Real Story

In February 2025, China introduced export licensing requirements for indium and several other critical materials. When the November 2025 United States-China trade deal paused export controls on gallium, germanium, and antimony, indium was deliberately left out. It is now the only one of the four export-controlled minor metals still under full restriction. China refines roughly 70 percent of the world's indium supply, in part because indium is recovered as a byproduct of zinc smelting and a large share of indium-bearing concentrates still go to smelters that lack the equipment to recover the metal. Supply does not respond to price signals on a meaningful timeline. Beijing decided which leverage points to keep, and indium was at the top of the list. The United States imports all of its indium and has never produced the material domestically.

Washington Is Building the Reserve, Slowly

In August 2025, the Defense Logistics Agency issued a request for information seeking 222 metric tons of high-purity indium ingots for the National Defense Stockpile. In April 2026, it followed with a contract solicitation worth up to 125 million dollars over three years. Indium prices have risen 27 percent in 2023, 23 percent in 2024, and roughly 19 percent through the first months of 2026, reaching decade highs. The European Union Critical Raw Materials Act and parallel United States programs have unlocked funding for mapping, recycling, and friend-shoring projects, but no primary production of indium exists or is on a near-term timeline domestically. Recycling and zinc-smelter retrofits are the only credible supply-side responses inside a five-year window, and both depend on capital expenditure decisions that have not been made. Executives planning artificial intelligence data center capacity through 2028 should price indium scarcity into procurement contracts now, before the next licensing tightening forces the conversation. Investors should treat any indium recycling, recovery, or substrate fabrication asset outside China as a strategic holding, with particular attention to the small group of zinc smelters in Canada, Belgium, and South Korea that have indium recovery infrastructure already operating. Policy makers should treat the November carve-out as a deliberate signal. Beijing held back the one mineral whose substitutes do not exist at scale and whose domestic United States supply chain has not yet been built, while releasing the three for which the United States has either alternative sources or active stockpile programs. That selection alone tells you which leverage point Beijing intends to use first, and the domestic stockpile build needs to move on a wartime timeline rather than a peacetime one. Service providers who advise clients with data center exposure should build indium dependency into the standard supply chain risk briefing immediately. It belongs alongside semiconductor, rare earth, and energy security in any serious enterprise risk register.

About Cambrian

Cambrian Futures is a strategic foresight and advisory firm helping government, business, and technology leaders understand how emerging technologies intersect with geopolitics, markets, and national strategy. By combining rigorous research, AI-enabled analysis, and human expertise, Cambrian provides clear insight into global technology trends, risks, and power dynamics. Its work helps decision-makers anticipate disruption, manage uncertainty, and act with strategic confidence in an increasingly competitive GeoTech world.

PRODUCTION TEAM

GeoTech Radar is produced by the Cambrian Futures Insights Platform team:

CEO & Chief Analyst

Managing Director / Producer, Insights Platform

Global Lead, Smart Infrastructure Strategy

Research & Marketing Associate

Editor in Chief

Learn more about Cambrian Futures at cambrian.ai

Produced with

Human Led

Human Led +

AI Augmented

AI Led +

Human Verified

Cite as: Cambrian Futures (2026) 'GeoTech Radar Issue 19'