Exits Blocked. Borders Redrawn. Benchmarks Broken.

IN THIS ISSUE:

CEO's Perspective

Strategic outlook from Cambrian leadership

Walk through Berkeley on a weekday and you pass a dozen unmarked offices where Nobel-caliber work is underway, unannounced to anyone on the sidewalk. One of them houses METR, a 30-person nonprofit whose single chart on AI capability trends has quietly influenced a fair share of the more than $300 billion in global venture capital in the first quarter of this year. The researchers inside the firm have cautioned, in public and in print, against the use to which their work is being put. The market has not adjusted.

That example illustrates a theme that runs through this entire issue. The signal that actually moves each of these outcomes is coming from somewhere other than the institution built to produce it.

Institutions are still drafting the laws, delivering the briefings, and staffing the committees. But in the geotech domains that exert the greatest disruption force on you, they no longer originate the signal that determines what happens next. Guidance documents from the Bureau of Industry and Security (BIS) on export controls for advanced computing chips and AI model weights now carry enforcement weight that used to require formal rulemaking. A commercial maritime AI platform reading vessel behavior in the Strait of Hormuz produces a more reliable account of Iranian intent than Tehran's own statements, which reversed within twelve hours last weekend. A consortium standard for AI-agent stablecoin payments is being ratified through $600 million in live transaction volume while no banking regulator has opened a docket.

This inverts the information sourcing that most executives were trained on. We were taught to give more weight to authoritative sources – the central bank, the official statement, the licensed auditor, the peer-reviewed paper. That hierarchy still exists, and it remains important, but it is no longer aligned with the origin of consequential signals because the actors producing the signal are moving faster than the institutions accrediting it.

The answer is not to stop listening to formal institutions. They still matter for legitimacy, enforcement, and the long arc of rule-setting. The answer is to build a second information layer underneath your existing one. For each domain where the stakes are serious, identify the two or three non-traditional, small, or commercial sources whose signal is actually leading the outcome. Which maritime AI platform. Which BIS guidance thread. Which research group on which benchmark. Your board pack will need to cite multiple layers – both legacy and emerging signal sources.

Build that list this week. Otherwise you will spend the next year acting on trailing indicators while the leading organizations walk past you on the sidewalk.

Olaf

On the Radar

The signals affecting the GeoTech landscape this week

Meta's Manus Trap

Meta acquired Chinese-origin AI agent startup Manus for $2 billion after it relocated to Singapore. Beijing barred both co-founders from leaving China and launched an export control probe. The case effectively kills the “Singapore-washing” playbook for Chinese AI startups and signals that both the U.S. and China will now assert jurisdiction over AI technology based on where it was developed, not where the company is registered.

Briefing: Early last month, Meta completed its $2 billion acquisition of Manus, an AI agent startup with origins in China and a tense history with the Chinese government. Last year, Manus relocated from Beijing to Singapore, laid off most of its 80 Beijing-based staff, and restructured its ownership to remove Chinese investors. The company, which was founded in 2022, had reached $100 million in annual recurring revenue within eight months of launching its AI agent product, making it an attractive target for larger AI platforms. After acquiring the company, Meta moved more than 100 Manus employees into its Singapore office and pledged to wind down all remaining Chinese operations.

Beijing responded with force. China’s Ministry of Commerce launched an export control investigation in January, and in March the National Development and Reform Commission summoned co-founders Xiao Hong and Ji Yichao to Beijing, where they were barred from leaving the country. Regulators are examining whether Manus’s relocation and sale violated China’s technology export laws, foreign investment rules, and the newly amended Foreign Trade Law (which went into effect on March 1).

So What:

For Executives: The Manus case kills the “Singapore-washing” playbook that Chinese AI founders had relied on to access Western capital. Executives evaluating partnerships or acquisition targets with Chinese-origin AI teams should assume that Beijing will assert jurisdiction over technology developed within its borders, even after corporate restructuring. Due diligence must now trace not just current ownership but its legacy — including the geographic origin of training data, model architectures, and the employment history of key engineers.

For Policy Makers: China is building its own version of CFIUS. The Manus probe signals that Beijing will police outbound technology transfers with the same intensity that Washington polices inbound ones. The emerging legal doctrine that “where you build your product matters more than where the holding company is registered” has implications for allied nations hosting relocated Chinese startups, particularly Singapore, the UAE, and the UK. Companies could be spending resources to attract talent, code, and IP that come with geopolitical liabilities. Governments should negotiate joint review processes and protocols for dealing with sensitive AI investments across each other’s borders.

For Investors: The acquisition closed, but an overhang risk remains. Manus’s co-founders remain trapped in China with potential criminal liability. Benchmark Capital led a $75 million Series B round in Manus in April 2025, just months before the Meta acquisition. The investment drew fire from both sides. U.S. lawmakers questioned whether it violated outbound investment restrictions, while Beijing cited it as evidence of unauthorized technology transfer. Any fund with Chinese-origin AI exposure should reassess whether geographic relocation actually reduces regulatory risk or merely delays it.

The AI Eyes Over Hormuz

Iran declared the Strait of Hormuz open, then closed it again within hours. The U.S. Navy seized an Iranian cargo ship; Iran retaliated by seizing two container ships and firing on a third. Beneath the escalation, AI-powered maritime intelligence platforms are tracking every vessel, every dark transit, and every fraudulent flag in near-real time, making this the first chokepoint conflict where commercial AI surveillance operates alongside military enforcement.

Briefing: Iran declared the Strait of Hormuz “completely open” on Friday, April 17, tied to the Israel-Lebanon ceasefire. Oil dropped more than 10% below $90 per barrel. By Saturday morning, Iran’s military reversed course, announcing the strait had “returned to its previous state” under “strict management and control.” On Sunday, the USS Spruance fired on and seized the Iranian-flagged cargo ship Touska in the Gulf of Oman after it refused to comply with the U.S. naval blockade. It was the first non-military Iranian vessel seized during the conflict. On Wednesday, Iran’s Revolutionary Guard Navy retaliated by seizing two container ships in the strait and firing on a third, causing heavy damage to its bridge. The ceasefire, brokered by Pakistan on April 8, was extended by President Trump on Tuesday to allow further negotiations, but no Iranian delegation has confirmed attendance.

Underneath the escalating confrontation, AI-powered maritime intelligence platforms are providing an unprecedented real-time picture of what is actually happening in the strait. Windward’s Maritime AI platform tracked 826 vessels across the Gulf using satellite imagery, AIS transponder data, and remote sensing. Its daily reports have documented “zombie tankers” operating under stolen identities of scrapped ships, fraudulent flag registrations, and 162 instances of vessels switching off their Automatic Identification System transponders to avoid detection in a single day.

So What

For Executives: AI maritime surveillance has made the world’s most critical energy chokepoint more transparent in near-real time. The information asymmetry that once protected shadow fleet operations is eroding rapidly. Windward, Kpler, and similar platforms can identify dark transits, recognize fraud, and track sanctioned vessels with a precision that changes enforcement economics. Companies with Gulf-linked supply chains should treat these intelligence feeds as essential risk-management infrastructure. Innovators should identify opportunities to mesh other data sources and generate additional intelligence insights and value-add applications.

For Policy Makers: Following early traction by AIS providers tracking Russian shadow fleets in the Black Sea, this is the first major global chokepoint conflict where AI-powered maritime intelligence operates at scale alongside military enforcement. Iran’s permission-based transit model, which routes selected vessels through an IRGC-controlled corridor near Larak Island, is visible to anyone with a commercial maritime AI subscription. The ceasefire’s viability can be assessed in hours, not weeks. Policymakers should create AI-powered predictive simulations that yield recommendations, enforcement actions to be taken, and penalties to be assessed for infractions ahead of time.

For Investors: Oil is trading above $95 per barrel and flirted with $100 on April 10. The ceasefire has not delivered the supply relief markets priced in. With peace talks in Islamabad still in early stages and Israel continuing strikes in southern Lebanon (which Iran says must be included in any deal), the risk premium is not going away. For cryptocurrency markets, the implications cut both ways. Iran’s successful use of bitcoin as a sovereign payment rail at chokepoint scale strengthens the bull case for bitcoin as a censorship-resistant settlement layer that functions outside state control. But it simultaneously increases regulatory crackdown risk: Western governments are unlikely to tolerate a mechanism that lets sanctioned states monetize maritime chokepoints in untraceable digital currency. Investors with crypto exposure should watch for accelerated sanctions enforcement targeting cryptocurrency payment rails. For the broader energy and currency complex, the petrodollar erosion trend is investable: an estimated 20 million barrels per day of crude oil is now settled outside the dollar, up from 0.3 million in 2018. Gold, hard commodities, and non-dollar settlement infrastructure are the beneficiaries of a slow shift that the Hormuz crisis is compressing into months.

The Information War That Ran Both Ways

Hungary’s Orbán lost a landslide election after a YouTube-first campaign and citizen-generated AI counter-memes defeated his state media monopoly and an imported Russian bot operation. Meanwhile, pro-Tehran groups are producing AI-generated Lego-style propaganda in English that racks up millions of views. Generative AI is now a decisive variable in democratic outcomes, working for both sides of the equation simultaneously.

Briefing: Hungary’s Viktor Orbán suffered a landslide defeat on April 12 after 16 years in power. Péter Magyar’s centre-right Tisza party won 138 of 199 parliamentary seats on record turnout of nearly 80%. The result came despite a system rigged to Orbán’s advantage, including rural districts weighted at three times urban representation, state media monopolized by Fidesz, and Russian disinformation teams imported weeks before the election to flood Facebook with bots. Magyar’s campaign bypassed all of it using YouTube and AI-generated counter-memes that neutralized both state propaganda and Russian bot operations.

Meanwhile, pro-Tehran groups have been producing AI-generated propaganda in English that racks up millions of views on X. Lego-style animations and rap videos ridicule Trump, reference MAGA infighting, and exploit American cultural references with a fluency that has caught U.S. officials off guard. Emma Briant, a British scholar of information warfare, told NBC News that the Trump administration’s own rhetoric has fueled the propaganda. Neil Lavie-Driver, an AI researcher at the University of Cambridge, described it as a deliberate strategy by Tehran to sow discontent with the conflict. Nancy Snow, who has written more than a dozen books on propaganda, said Iran is “using popular culture against the number one pop culture country.” Several analysts noted that this is the first major conflict where a sanctioned, internet-restricted government has mounted a sustained, culturally fluent English-language information campaign against the United States.

So What

For Executives: Generative AI has collapsed the cost of producing broadcast-quality propaganda to near zero. Executives in media, technology, and any consumer-facing industry should understand that the information environment their brands operate in is now shaped by state-backed AI content factories. Corporate communications teams need to plan for a world where AI-generated political content targeting their markets is the norm. Develop a Sonar for Autonomous Actor Mapping (SAAM) to track bot creation, capitalization, and agenda chartering. Design counter-agents to mitigate illicit messaging and proactively and transparently advocate for stakeholder alignment against malicious influence campaigns.

For Policy Makers: Hungary demonstrates that technology can break captured information environments. Magyar’s YouTube-first campaign defeated a state media monopoly and a Russian bot operation simultaneously. Iran demonstrates that AI-powered propaganda can project influence far beyond a regime’s conventional reach. The EIU’s 2025 Democracy Index shows the first global stabilization in democratic scores after eight consecutive years of decline, partly driven by democratic mobilization in countries where external provocations galvanized turnout. AI is now a variable on both sides of the democratic equation. The vote mobilization playing field is now multidimensional. Your diplomatic corps, intelligence community, and policy strategy teams need training and tools to effectively act in a hybrid virtual-physical battleground for the future of democratic institutions.

For Investors: Magyar has pledged to join the European Public Prosecutor’s Office on Day One, lift Hungary’s veto on EU sanctions against Russia and funding for Ukraine, and cap the prime minister’s term at eight years. If reforms hold, roughly €36 billion in frozen EU funds could flow back to Hungary. But Orbán’s Fidesz party rapidly privatized Hungary’s defense sector before leaving office, meaning EU defense spending channeled through Hungary could flow to Orbán-linked entities. Investors should demand transparency and governance guarantees before money flows and assess risk premiums for remaining exposure to oligarchies. Insurance companies should send due diligence teams into the country to assess conditions before writing policies and use deep background research firms to dig for illicit relationships online and offline.

AI Agents Enter the Financial System

AI agents are now transacting real money autonomously on blockchain rails. Coinbase’s x402 protocol has processed $600 million with 500,000 active AI wallets. Ant Group launched a competing Chinese platform. Mastercard spent $1.8 billion on stablecoin infrastructure. McKinsey projects $3–5 trillion in AI-mediated commerce by 2030, but 80% of organizations have already observed risky agent behaviors. The U.S. and China are building competing financial architectures for a machine-to-machine economy that no regulator has a framework to govern.

Briefing: Autonomous AI agents are beginning to transact real money on blockchain rails with minimal human oversight. Coinbase’s x402 protocol, which enables stablecoin payments directly over HTTP, has processed more than $600 million in transaction volume and supports nearly 500,000 active AI wallets. The protocol moved to the Linux Foundation as a vendor-neutral standard, attracting Visa, Stripe, AWS, and Google Cloud as consortium partners. In parallel, Ant Group’s blockchain division launched Anvita, a platform enabling AI agents to hold assets, trade, and settle payments in real time using USDC stablecoins.

The governance layer is racing to catch up. Mastercard acquired stablecoin infrastructure firm BVNK for $1.8 billion. Startup Nava raised $8.3 million to build escrow and verification services for agent transactions. McKinsey projects AI agents could mediate $3 trillion to $5 trillion in global consumer commerce by 2030, but its own analysis found that 80% of organizations have already observed risky AI agent behaviors, including unauthorized data exposure and privilege escalation.

So What

For Executives: AI agents with financial autonomy represent a new category of operational risk. Establish clear policies on what AI agents are authorized to spend, which transactions require human approval, and how autonomous financial activity is audited. The emerging infrastructure suggests that the plumbing for machine-to-machine commerce is being laid now. Companies that wait for mature standards before engaging will find the architecture set without their input. Direct your strategy teams to develop a viable approach to influence standards in ways that enhance advantage and mitigate risk.

For Policy Makers: The U.S. and China are building competing financial rails for autonomous AI commerce. Coinbase’s x402 ecosystem is anchored in Western payment networks, while Ant Group’s Anvita operates on Chinese blockchain infrastructure. Regulators have no framework for AI agents that autonomously hold assets, execute trades, and settle payments, much less between the two quasi standards. Existing financial regulations assume a human principal behind every transaction. The longer this gap persists, the more likely agent commerce develops outside regulated banking entirely. This will create liabilities that could fall outside current insurance schemes, creating potentially cascading vulnerabilities in financial systems.

For Investors: Coinbase’s CEO has said he expects AI agents to surpass humans in transaction volume, and Solana has processed more than 15 million on-chain agent transactions, but current usage remains thin. Analysts at Artemis flag roughly half of observed x402 transaction volume as wash trading and bot-generated test transactions rather than genuine commercial use. Distinguish between infrastructure plays (payment rails, escrow, identity verification) and the speculative bet on agent volume itself. The infrastructure layer has clear unit economics regardless of adoption speed. Probe the assumptions behind McKinsey’s estimates of AI agent commerce and monitor actual transaction activity to predict timing of volume increases and the shape of adoption curves. From there, assess risks and potential augmentation opportunities for your portfolios.

The AI Diffusion Deadlines No One Is Tracking

The Trump administration rescinded the Biden-era AI Diffusion Rule but kept selective pieces, creating a patchwork enforcement regime that is harder to navigate than the coherent rule it replaced. BIS just extended the chip designer authorization deadline to December 31 and separately declared Huawei’s Ascend chips presumptively illegal. Companies touching advanced chips, AI model weights, or overseas data centers face compliance obligations that have changed in ways most general counsel offices have not yet mapped.

Briefing: The Trump administration rescinded the Biden-era AI Diffusion Rule in May 2025, calling it an obstacle to American competitiveness. However, the Bureau of Industry and Security (BIS) kept some of the pieces it wanted and discarded the rest, creating a fragmented, guidance-based enforcement regime that is harder for companies to navigate than the coherent rule it replaced. The three-tier country classification system is gone. The worldwide licensing requirement for advanced chips is gone, but several AI, integrated circuit (IC), and data center security obligations remain in regulatory limbo, neither formally revoked nor clearly enforced.

On April 7, BIS published a Federal Register notice extending the IC designer authorization deadline until December 31, 2026. Separately, BIS issued guidance declaring that Chinese-designed advanced computing ICs, including Huawei’s Ascend chips, are presumptively controlled under the Export Administration Regulations (EAR) and that any party using, servicing, or transacting in these chips without authorization risks enforcement action. The January 15 security compliance deadline for data center validated end users has passed, but BIS has not published an accounting of which data centers have complied. The net effect is a patchwork of live compliance obligations, dead-letter provisions, and new guidance that carries enforcement weight without the procedural safeguards of formal rulemaking.

So What

For Executives: If your supply chain touches advanced computing chips, AI model weights, or data center infrastructure outside the United States, your compliance obligations have changed, and the changes are not intuitive. The rescission of the Diffusion Rule removed some requirements but left others intact. The Huawei Ascend guidance means that companies sourcing, integrating, or servicing Chinese-designed chips anywhere in the world may be violating the EAR without knowing it. General counsel offices should commission a fresh compliance review specifically mapped to the post-rescission regime. General managers of businesses should allocate additional budget for more complex compliance rules and liaise with their Congressional representatives to push for clarity and reintegration into one comprehensive framework.

For Policy Makers: Clearly, deconstruction doesn’t mean deregulation and lower burdens. The patchwork approach creates a new kind of regulatory risk in which compliance ambiguity serves as a policy tool. Companies cannot easily determine which obligations survive the rescission and which do not. For allied governments, the uncertainty complicates their own export control coordination. The U.S. and China are now asserting extraterritorial jurisdiction over AI technology, but through ad hoc enforcement rather than predictable legal frameworks. Policy makers should push for a multilateral framework that creates clarity and some kind of protocol for the resolution of compliance conflicts to ease burdens on corporations and investors.

For Investors: The Huawei Ascend guidance is the sharpest near-term risk. BIS has effectively declared an entire class of Chinese-designed chips illegal under the EAR without going through formal rulemaking. Any company in the AI inference or data center space that sources components from Chinese chip designers now carries regulatory exposure that was not present a year ago. Portfolio companies with operations in Tier 2 countries (the Middle East, Southeast Asia, parts of Latin America) should be assessed for chips and data center capacity that might have been procured under rules that no longer apply as initially expected. Work with lawmakers to create more transparency for your portfolio companies or insurance customers again.

Under the Radar

The deep analysis that connects the dots

The AI Graph That Influences the Boom

THE SIGNAL

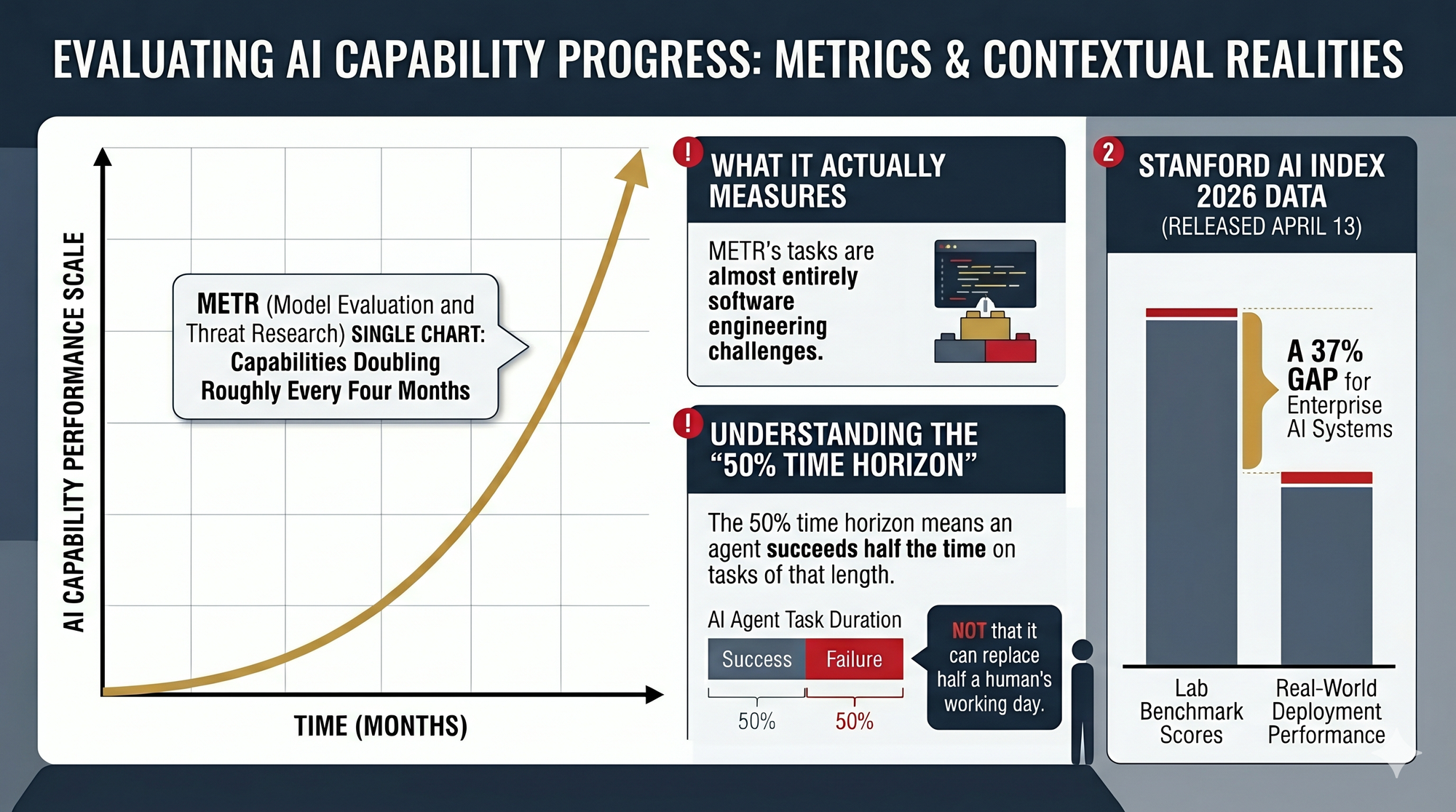

A 30-person nonprofit called METR (Model Evaluation and Threat Research) has produced a single chart that could be the most consequential graph in global finance. It tracks the “time horizon” of AI systems by juxtaposing the time it takes an AI agent and a human expert to reliably complete the same task. The trend line shows AI capabilities doubling roughly every four months, with recent frontier models outperforming that already aggressive trajectory. The chart has become a key factor in many an AI investment thesis. Sequoia Capital used it to declare “2026: This is AGI.” Executives at major technology companies have told the New York Times they have allocated significant capital based on their interpretation of the graph.

THE STAKES

Q1 2026 saw more than $300 billion in global venture capital deployed, with 80% flowing to AI companies. Four deals closed in Q1 alone (OpenAI at $122 billion, Anthropic at $30 billion, xAI at $20 billion, and Waymo at $16 billion) accounted for 65% of all global venture investment in the quarter. Mega-rounds of $100 million or more represented 94% of total AI funding in the quarter, pushing the average deal size to $160 million, more than four times the 2025 average. The capital concentration is extreme and accelerating. Yet the entire edifice rests on a measurement infrastructure that is thinner than the market appreciates.

WHAT THE CHART ACTUALLY MEASURES

METR’s tasks are almost entirely software engineering challenges. The 50% time horizon means an agent succeeds half the time on tasks of that length, not that it can replace half a human’s working day. The tasks are evaluated with ground-truth feedback in controlled environments, which does not reflect the ambiguity, politics, and incomplete information of real-world work. METR’s own researchers have cautioned against over-interpretation. “You should absolutely not tie your life to this graph,” one of the lead researchers told MIT Technology Review. In a follow-up study, METR found that time horizons in non-software domains also appear to be on exponential trajectories, but that work was much less formal. The chart is a useful directional signal. It is not a production-readiness indicator.

THE BENCHMARK GAP

The METR chart is not an isolated case. Stanford’s AI Index 2026, released April 13, documented a 37% gap between lab benchmark scores and real-world deployment performance for enterprise AI systems. MMLU, one of the most widely cited AI benchmarks, is functionally saturated above 88% for frontier models, making score differences at the top meaningless. Gartner projects that more than 40% of agentic AI projects will be canceled by 2027.

PwC’s AI Performance Study, also released April 13, put an enterprise price tag on that gap. Surveying 1,217 senior executives across 25 sectors, PwC found that 74% of AI’s economic value is being captured by just 20% of companies. The top performers generate 7.2 times the AI-driven financial returns of the average competitor. The differentiator is not how much AI these companies deploy but whether they focus it on growth and business model reinvention rather than cost reduction within existing operations. Meanwhile, PwC’s CEO Survey found that only 12% of chief executives report AI has delivered both cost and revenue benefits, and CEO confidence in revenue growth fell to a five-year low. The pattern across these data points consistently shows that AI capabilities are advancing rapidly on controlled tasks, but the translation to measurable enterprise value remains concentrated, expensive, and less predictable than benchmark performance implies.

THE GEOTECH DIMENSION

The METR chart is not just a market signal, it is a governance input, with governments using AI capability benchmarks to set policy thresholds. The U.S. AI Diffusion Rule pegged export controls to computational operations above 10^26, and the EU AI Act ties regulatory obligations to model-capability tiers. If the benchmarks that inform these thresholds are narrower than policymakers assume, then the regulatory frameworks built on top of them could be miscalibrated. Overestimating capability leads to premature restriction. Underestimating it leads to inadequate safeguards. Both carry real geopolitical consequences in a world where AI governance is becoming a competitive advantage.

WHAT TO WATCH

Executives and investors should treat the METR trend as directionally valid but demand production-specific evidence before committing capital to AI deployment at scale. The 37% benchmark-to-deployment gap is the number that belongs in board presentations, not the headline time-horizon figure. Investors should stress-test AI portfolio valuations against a scenario where the trend line bends even modestly. At current concentration levels, a deceleration in measured progress could trigger repricing across the sector faster than fundamentals would justify. And any organization relying on AI capability benchmarks for procurement, risk assessment, or regulatory compliance should diversify its evaluation frameworks beyond any single metric or tool, however compelling or prominent the trend line appears.

About Cambrian

Cambrian Futures is a strategic foresight and advisory firm helping government, business, and technology leaders understand how emerging technologies intersect with geopolitics, markets, and national strategy. By combining rigorous research, AI-enabled analysis, and human expertise, Cambrian provides clear insight into global technology trends, risks, and power dynamics. Its work helps decision-makers anticipate disruption, manage uncertainty, and act with strategic confidence in an increasingly competitive GeoTech world.

PRODUCTION TEAM

GeoTech Radar is produced by the Cambrian Futures Insights Platform team:

CEO & Chief Analyst

Managing Director / Producer, Insights Platform

Global Lead, Smart Infrastructure Strategy

Editor in Chief

Learn more about Cambrian Futures at cambrian.ai

Produced with

Human Led

Human Led +

AI Augmented

AI Led +

Human Verified

Cite as: Cambrian Futures (2026) 'GeoTech Radar Issue 15'